Home » Taxes

Category Archives: Taxes

Of Tax Breaks and Budget Holes

(Recent letter to the editors of my local newspapers)

Dear Editor:

I don’t think most people in New Jersey get it yet. When politicians tell us revenue collected for a better 911 system had to go for other law enforcement priorities, they aren’t being honest. Their “spending priorities” mask tax revenue lost to off budget deals for special interest tax breaks. These special tax breaks loosely translate into campaign donation or political clout for New Jersey politicians.

Special tax deals don’t show up as a liabilities on a budget line. They show up as holes in the budge that must be plugged. They show up as insufficient revenue to pay for state pensions, or daycare assistance, or NJ Transit funding, or the Transportation Trust Fund. Every time a dedicated funding stream is raided to plug a spending gap we should demand to know what created the revenue gap in the first place.

I believe we are intentionally distracted by dramatic spending conflicts to conceal the real action behind the revenue side of the ledger. It’s time to claw back all those special interest tax breaks and make the rich and powerful pay their fair share of taxes. Let’s require that all future budges contain a detailed accounting of all the tax breaks currently in effect.

Brian T. Lynch

Note: The readers of this blog are free to copy this letter or model their own letter after it to send to their own local newspapers.

A few other points that had to be left out:

- The tighter the state or municipal budget the greater the disparity between those who pay the taxes they owe and those who cheat on their taxes or get special interest tax breaks. Unfair taxation is at the root of revenue shortfalls.

- The article makes the point about wealthy corporations and the rich, because they have the means to make cheating on taxes legal (special interest tax loop holes). They also pay the least amout of taxes relative to their income and wealth. But the tax revenue drain also comes from a growing underground cash economy. Just the other day a buildings trade contractor told me he would lower an estimate if I paid cash (I declined).

- No matter where people fall on the wealth and income spectrum they feel cheated by a tax system that allows others to pay less than their fair share. Everyone feels entitled to cheat a little on their taxes. Today, cleaver manipulation of the tax code to avoid paying even massive amounts of federal taxes is admired. This is a far cry from when the current progressive tax code was first implemented 101 years ago. Paying taxes was considered a patriotic duty. Considering how strongly people voice their support for our military, coupled with the fact that nearly 50 cents of every federal income tax dollar goes to the military, you would think that it would still be patriotic to pay taxes today.

OR AT LEAST YOUR FAIR SHARE OF TAXES

Tax Breaks are the Rigging in a Rigged System

by Brian T. Lynch, MSW

(A letter to the editor I submitted today. Please feel free to copy and send to your own local editors without attribution.)

Dear Editor:

Have we all lost our minds? Have we all forgotten that special interest tax loopholes are a tax burden for the rest of us? Are we so jaded that we no longer see tax breaks as evidence of political corruption?

Who among your readers would vote for a special tax break knowing it would raise their own taxes? If the majority ruled, as it should in our Republic, most tax breaks wouldn’t exist.

While Trump and his supporters say how genius it is of him to so cleverly exploit these disgusting loopholes, wouldn’t the financial gains of a corruptly created tax breaks also be tainted?

Muck money! Graft booty! We don’t have a precise word for it, but exploiting ill gotten tax breaks for personal gain isn’t honorable. It is unfair. It is the rigging in a rigged system. Tax loopholes may be legal but that doesn’t make them respectable.

No Fairness in Funding NJ Public Schools

by Brian T. Lynch, MSW

Fairness Formula? Governor Chris Christie is proposing a plan to give an equal amount of State Aid funding to every student in every school districts in New Jersey. Specifically, his proposal would take the higher amounts of State Aid we currently give to very poor districts and distribute it equally across the state to reduce property taxes in the wealthier suburbs. This, he says, is fair.

For those who are not familiar with New Jersey, most school funding is raised through a local wealth tax based on the assessed value of residential and private property. This is a highly regressive way to raise revenue, as you will see below.

We are big on home rule in New Jersey, so each town has its own independent school board. Each towns Board of Education proposes an annual school budget which is voted on in a public referendum. If passed, the costs are incorporated into the municipal budget and property tax rates are raised if more revenue is needed. If the school budget fails, town and school officials have to either cut the school budget or make other adjustments to municipal services so property taxes don’t rise.

Here is truism: Wealthy municipalities tend to grow more affluent over time while poor districts tend to decline even further.

Wealthy towns have better school systems in New Jersey. That is also a fact. So parents who can afford to upgrade their home often move into towns with better schools. Property values rise with the demand for homes in districts with better schools. Property values decline in districts that have underfunded or troubled schools, so property tax rates must increase in poor districts just to break even on current school spending. As property values increase in wealthy districts, more property tax revenue is generated. Some of this additional revenue goes into further improving the schools without the need to increase taxes. In some cases tax rates may even decline in affluent municipalities as home values rise. The result is that wealthy districts have much better public schools and lower tax rates while poor districts cannot afford to keep up the disadvantaged schools they have.

State Municipal and School Aid was designed to help level municipal tax burdens in New Jersey. State Aid is allocated to local municipalities and school districts to fill in the gaps that exist between wealthy and poor municipalities. This funding solution grew out of a state Supreme Court ruling, Abbott vs. Burke, that found New Jersey school funding did not result in equal education opportunity, as mandated by the State Constitution.

This vicious cycle of migration between rich and poor districts is a big reason for the educational funding disparity. It is the one usually mentioned by NJ state legislators and the press. But this cycle only exacerbates an underlying funding flaw. A wealth tax based on residential property values is incredibly regressive.

I wrote another article about the regressive education taxes in New Jersey last year. The Governor’s new School Aid plan only compounds the problem.

To show just how unfair residential wealth taxes are for funding public schools, consider that people who own million dollar homes almost always have significant other wealth investments and ownership interests that aren’t being taxed to funding public schools. The rich have far more wealth and investment income. On the other hand, people who own homes in economically depressed areas, people whose homes are well below the state average in value, have few investments or ownership stakes. Many of them have a negative net worth, almost no savings and many of them struggle to pay their monthly bills.

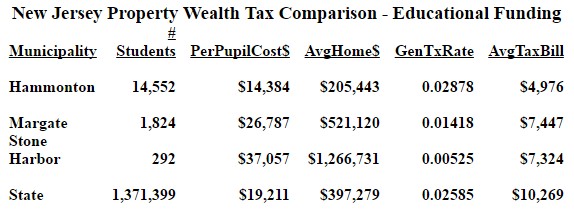

Most economists agree that a flat tax is a regressive tax. It favors the rich, but it is still far less regressive than the property tax scheme in New Jersey. To illustrate, the table below looks at information from three actual New Jersey municipalities: a poor district, an modestly affluent district and a wealthy district. The number of students in these districts tell you that these aren’t all K-12 districts, but the tax lesson here is still valid whether a district is a sending district or not.

| Table 1 |

Hammonton and Margate are municipalities in Atlantic County and Stone Harbor is in Cape May County. In all three districts the average tax bill is below the state average. Hammonton does a pretty good job of keeping per pupil costs down so it’s residents can afford their property taxes. It is a town where the average home value of $205k is significantly below the state average of nearly $400k. It is not an affluent community like Margate, or a wealth district like Stone Harbor where the average home sells for over a million dollars.

The average tax bill in Hammonton is just under $5,000 per year, almost half the state average. The $14,384 annual per/pupil cost of education is also below the $19,211 state average. The low tax bill per resident is due, in part, to the fact that Hammonton receives $20 million dollars in State Aid.

Despite all of their frugal budgeting to keep tuition costs down, and despite a good amount of state assistance, look at Hammonton’s general property tax rate. It is double the tax rate in Margate and more than five time higher than the tax rate in Stone Harbor. Hammonton’s property tax rate is still well above the state average.

The residents of Margate and Stone Harbor pay a few thousand dollars more per year in property taxes, but they can well afford it. They pay less than the state average in property taxes yet spend far more than average in student tuition. Even so, Margate currently receives $2.5 million in State Aid while the very wealthy Stone Harbor receives nearly a half-million dollars in State Aid. Ironically, Under Governor Christie’s plan, each of these three districts would receive substantially more State Aid, but this would come at the expense of the very poor urban districts, the so call “Abbott” districts, where poverty levels are very high and property values are very low.

If instead of a flat State Aid rate for every student, Governor Christie proposed a flat property tax rate, and used additional revenue from wealth districts to fill funding gaps in poorer districts, how would that effect property taxes in these three communities?

Keeping in mind that a flat tax is still regressive, and that home values are not a good indicator of wealth ownership (it under represents the wealth of the wealthy) the table below shows what property taxes would look like if a flat property tax was implemented based on New Jersey’s average property tax rate.

Table 2

This exercise illustrates just how incredibly regressive the current property tax scheme is. More affluent towns are paying a lower property tax rate and middle class communities are paying a higher rate. Even a flat property tax rate would double Margate’s tax bill and more than quadruple Stone Harbors tax bill. A flat property tax rate would probably generate enough additional revenue to adequately fund and rehabilitate Abbott district schools and disadvantaged schools throughout the state. A progressive property tax formula would go even further to fully fund New Jersey’s public schools and give every child their constitutionally protected right to an equally good public education. Giving the same amount of state aid to both the rich and poor isn’t fair at all. A progressive wealth tax based on residential property values would be.

Below are the URL internet addresses for all of the data presented above.

_____________________________________________________________

http://www.nj.com/education/2015/04/nj_schools_how_much_is_your_district_spending_per.html

http://www.nj.gov/education/data/fact.htm

http://www.state.nj.us/education/data/enr/enr14/stat_doc.htm

http://www.state.nj.us/treasury/taxation/lpt/taxrate.shtml

http://www.state.nj.us/treasury/taxation/lpt/class2avgsales.shtml

http://www.joeshimkus.com/NJ-Tax-Rates.aspx

http://www.state.nj.us/dca/divisions/dlgs/resources/stateaidinfo.shtml

A Silent Rage Approaching

by Brian T. Lynch, MSW

The rich are not like you and me. I can safely say that knowing they’ll never read this.

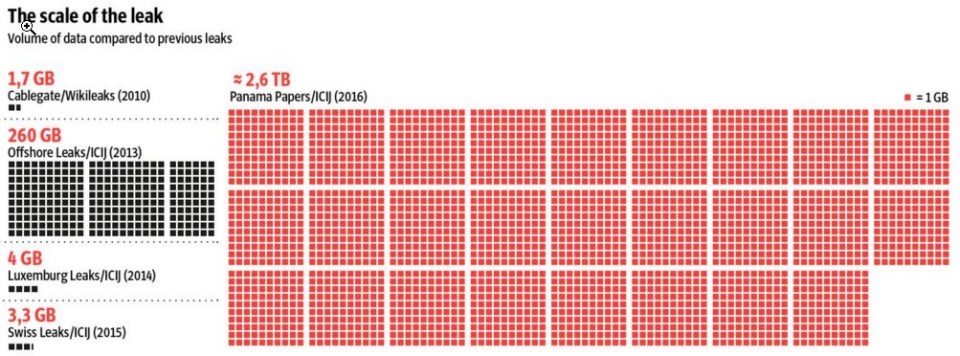

The massive leak of documents from the Panamanian law firm Mossack Fonseca shows the extent to which the global elite shield their wealth from us. They have no interest in sharing the cost of governing. We pay for the military, the courts, the police, the roads, the schools and all of our social and physical infrastructure. The wealthy mooch off of us by not paying their taxes. The system is rigged to benefit those who least need the benefits. Some of the tax dodges are written into the law by politicians deep within the pockets of the rich. But as the Panama Papers reveal, most of the unreported wealth is hidden illegal. All of it is underhanded and immoral.

The sheer number of documents leaked is enormous. It covers 40 years of financial transactions and 2.6 terabytes of data. If media coverage of this scandal were proportional to the size of the document cashe, there would be no other news on television for weeks. Here below is a graphic depiction of the scale of the leak compared with other huge scandalous leaks.

As it stands, the owners and share holders of our corporate media are likely involved somewhere in this scandal. If not them directly, then surely their customers who buy advertizing are caught in this vast net of stinking fish. The hard working, front line journalists responsible for turning this data mountain into intelligible information have little control over how their work will be broadcast. For now, at least in the United States, coverage of the scandal is trumped by presidential politics.

If our society were healthy, if so many of us had not already given up on government’s lack of responsiveness to public demands, this would be a watershed moment. It would be a tipping point for righteous indignation and hot pursuit of substantial reforms.

The wealthy will tell you their fair share is in the paltry proportion they do pay in taxes, but the proof of the lie is the growing number of children living in poverty whose benefits are cut by the budget knife. The proof of the lie is in our crumbling bridges and crowed roads that we can’t fix without killing off other essential services. No matter how big some people say government is, it’s too small and corrupted to make these powerful people pay all their taxes.

It is all too depressing. All the more so if you believe, as I do, that a failure to mobilize for real change now puts the world on the path to real revolution, bloodshed and destruction. It is a well documented historical pattern, just as inevitable yet avoidable as global warming. It has happened countless times before, except this is different. This time tearing down our institutions in a murderous fit of rage would likely condemn the Earth to mass extinctions.

As much as we rail against the “system” we need it for the higher level of coordination and cooperation it will take to solve the global catastrophe we face. We can’t solve these challenges without reforming our current power structures and the eliminating the barriers created by greedy capitalists. Only the collective power of our vast social institutions can bring about the kind of changes we must make to survive. Radical reform is our best option for survival. How do we get a critical mass of people to understand this before it is too late?

The Panama Papers Scandal Parses the Difference Between Bernie and Hillary

by Brian T. Lynch, MSW

This is yet another example where a clear eyed, independent Bernie Sanders warned against passing legislation that he knew would be disastrous while Hillary Clinton pressed for its passage. Sanders said exactly what would happen if the Panama free trade agreement passed. He said it would make it easier for, ” … the wealthiest people and most profitable corporations in this country to avoid paying their fair share in taxes by setting-up offshore tax havens in Panama.

Today we read headline stories like this:

“Years before more than a hundred media outlets around the world released stories Sunday (April 3, 2016) exposing a massive network of global tax evasion detailed in the so-called Panama Papers, U.S. President Barack Obama and then-Secretary of State Hillary Clinton pushed for a Bush administration-negotiated free trade agreement that watchdogs warned would only make the situation worse.”

After the free trade agreements passed in Congress, then Secretary of State Hillary Clinton released the following statement:

“The Free Trade Agreements passed by Congress tonight will make it easier for American companies to sell their products to South Korea, Colombia and Panama, which will create jobs here at home. The Obama Administration is constantly working to deepen our economic engagement throughout the world and these agreements are an example of that commitment.

Source: https://blogs.state.gov/stories/2011/10/13/passage-colombia-panama-and-south-korea-trade-agreements

In opposition to the Panama free trade agreement bill being debated in the Senate, Bernie Sanders said this on October 12, 2011 (Panama comments printed here in full) :

Finally, Mr. President, let’s talk about the Panama Free Trade Agreement.

Panama’s entire annual economic output is only $26.7 billion a year, or about two-tenths of one percent of the U.S. economy. No-one can legitimately make the claim that approving this free trade agreement will significantly increase American jobs.

Then, why would we be considering a stand-alone free trade agreement with this country?

Well, it turns out that Panama is a world leader when it comes to allowing wealthy Americans and large corporations to evade U.S. taxes by stashing their cash in off-shore tax havens. And, the Panama Free Trade Agreement would make this bad situation much worse.

Each and every year, the wealthy and large corporations evade $100 billion in U.S. taxes through abusive and illegal offshore tax havens in Panama and other countries.

According to Citizens for Tax Justice, “A tax haven . . . has one of three characteristics: It has no income tax or a very low-rate income tax; it has bank secrecy laws; and it has a history of non-cooperation with other countries on exchanging information about tax matters. Panama has all three of those. … They’re probably the worst.”

Mr. President, the trade agreement with Panama would effectively bar the U.S. from cracking down on illegal and abusive offshore tax havens in Panama. In fact, combating tax haven abuse in Panama would be a violation of this free trade agreement, exposing the U.S. to fines from international authorities.

In 2008, the Government Accountability Office said that 17 of the 100 largest American companies were operating a total of 42 subsidiaries in Panama. This free trade agreement would make it easier for the wealthy and large corporations to avoid paying U.S. taxes and it must be defeated. At a time when we have a record-breaking $14.7 trillion national debt and an unsustainable federal deficit, the last thing that we should be doing is making it easier for the wealthiest people and most profitable corporations in this country to avoid paying their fair share in taxes by setting-up offshore tax havens in Panama.

Adding insult to injury, Mr. President, the Panama FTA would require the United States to waive Buy America requirements for procurement bids from thousands of foreign firms, including many Chinese firms, incorporated in this major tax haven. That may make sense to China, it does not make sense to me.

Finally, Panama is also listed by the State Department as a major venue for Mexican and Colombian drug cartel money laundering. Should we be rewarding this country with a free trade agreement? I think the answer should be a resounding no.

It is very difficult for average citizens like me to see clearly what our politicians are really up to. This is true in part because we no longer have an independent press challenging our politicians pro-business policies. If “free trade” is good for businesses and the wealthy (the donor class), it’s good for corporate media profits and for campaign funding PAC’s.

It is this nexus between business, politics and the media that form the self-interested “establishment” in America. It is a ruling elite that competes with itself along party lines without faithfully serving the interests of ordinary citizens. Both the extraordinary outsider presidential campaigns of Donald Trump and Bernie Sanders are driven by this single aspect of our national polity, the establishment elite.

Donald Trump representing opposition to the Republican flavor of the establishment elite. He thrashes about like a wild man trying to cobble together a rage tag constituency of the disillusioned on the right.

Senator Sanders, on the other hand, has always seen through the self-serving positions of the New Democrats (or Third Way Democrats). The centrist moves of the modern Democratic party has always been a slide towards corporate power. It helps Democrats win elections because centrist positions are more lucrative for Democratic campaigns. By not accepting PAC money or wealthy donations, Bernie Sanders has demonstrated just how clearly good politicians can see the true impact of proposed legislation.

In this and many other examples, Bernie Sanders is like a prophet. Not the religious kind, but in the secular sense. He sees where we are headed more clearly than most and then uses that information to try and get us to change course. That is what prophets, and parents and true statesmen do.

Coal Ash Disaster Turns Capitalists into Socialists (Again)

by Brian T. Lynch, MSW

Commentary:

Coal ash is what’s left after coal is burned. It’s a toxic stew containing heavy metals including arsenic, lead and mercury. For many years Duke Energy has mixed coal ash with water and pumped this cocktail from coal fired power plants into huge open pits. In February, one of the sludge pits located in North Carolina began releasing millions of gallons of toxic coal ash into the Dan River, a source of public drinking water for thousands of people.

Photo and article: http://www.salon.com/2014/02/26/north_carolina_might_finally_crack_down_on_duke_energy_after_disastrous_coal_ash_spill/

Duke Energy spent millions over the years to keep government from properly regulating their waste products. For all those decades the stockholders and upper management of Duke energy have profited from this arrangement. Now that the inevitable has occurred, clean up effort will take years and cost a billion dollars. Millions more will have to be spent to correct the improper disposal problems that Duke Energy has practiced for decades.

Safely storing coal ash should have been a cost of doing business for Duke Energy all along, but they have deferred that cost to boost their profits. Now Duke Energy’s president and CEO, Lynn Good, thinks taxpayers should bear the cleanup costs. She said, “Ash pond closure has been a plan for very long time. And because that ash was created over decades for the generation of electricity, we do believe that ash pond disposal costs are ultimately a part of our cost structure.” She believes the burden of this clean up should be shared by everyone equally. (Corporate socialism? Again?)

Corporation are legally obligated to maximize profits for their shareholders. This would be fine if they were also legally obligated to paid the full cost of doing business without cutting corners. Cleaning up toxic spills is far more expensive than preventing themand regulations to enforce safe disposal are less expensive in the long run. But asking the victims of their environmental crimes to pay for cleaning up their mess and fixing their problem should not be an option.

(See also: http://www.politicususa.com/2014/03/14/republican-hypocrites-force-nc-taxpayers-pay-duke-energys-toxic-coal-ash-dumping.html )

Immigration Myths Hide the Benefits Says US Chamber of Commerce

From the US Chamber of Commerce: This ultra-conservative organization finally comes clean with a DATA DRIVEN VIEWPOINT support their position on immigration and how it benefits the US economically. http://www.scribd.com/doc/179652570/Immigration-Myths-and-Facts

Immigration Myths and Facts

Despite the numerous studies and carefully detailed economic reports outlining the positive effects of immigration, there is a great deal of misinformation about the impact of immigration. It is critical that policymakers and the public are educated about the facts behind these fallacies. [Says the US Chamber of Commerce]

Below I present the major points of their arguments. Please go to their website to read a detailed explanation for each of these points.

JOBS MYTH: Every job filled by an immigrant is a job that could be filled by an unemployed American.

Bogus Claim: Obama Uses IRS to Buy Votes

There appears that a phony new scandal is taking shape on some conservative corners of the internet. It may or may not gain traction, but it is worth a peek. David DeVine, on the Website entitled TheWestern Free Press, and others, are accusing President Obama of using the IRS to create “de facto amnesty” for illegal aliens. It has to do with an aspect of federal tax law that has been ignored for years.

Here is the actual claim:

ITIN amnesty scam empowers Obama IRS to buy votes

“Outraged that illegal aliens claimed child-tax-credits, but no outrage that current tax law allows them to report income and pay taxes without threat of deportation?”

Apparently some on the right have finally discovered that many resident aliens actually do have IRS identification numbers that allow them to file and pay their federal income taxes and receive some tax benefits.

For years now rightwing conservatives have complained that undocumented aliens (by which they usually mean all non-citizens of color) don’t pay taxes and are a burden to taxpayers. This has never been entirely true, of course. Even setting income taxes and payroll deductions aside, all resident aliens pay sales taxes, property taxes (sometime indirectly by paying rent), gas taxes, cigarette taxes, tolls, fees , etc. But the biggest misconception has been that most resident aliens don’t pay income taxes. Many, perhaps most resident aliens do pay income taxes. Even my liberal friends have had a hard time believing this.

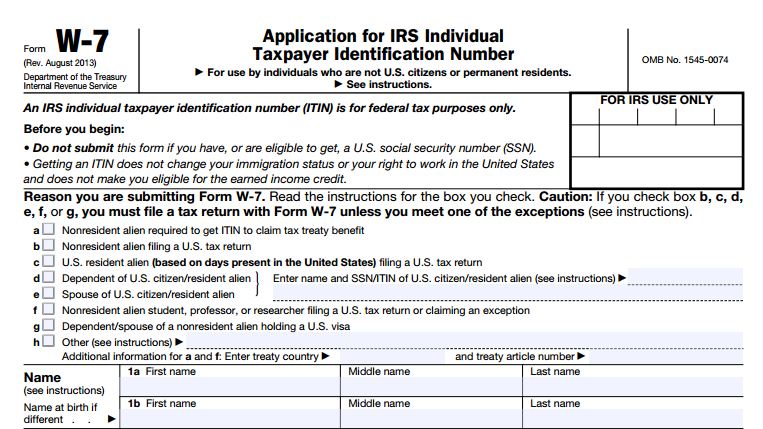

For more than forty-years the IRS has issued a nine-digit Individual Taxpayer Identification Number ( IRS application form W-7) to resident aliens who are not eligible to apply for Social Security. These identification numbers may be issued to resident aliens who earn income in the U.S. and either have a “Green Card” eligibility or meet the “Substantial Presentence” eligibility test. In fact, the instructions on the W-7 states, “A foreign individual living in the United States who does not have permission to work from the USCIS, and is thus ineligible for a SSN, may still be required to file a U.S. tax return”, and therefore obtain an Individual Taxpayer Identification Number (ITIN). So regardless of how a foreign citizen came to be here, if they earn money while here they are required to file income taxes. For example, a foreign citizen who came here in January and earned money and is still here in December must file income taxes and apply for the ITIN by attaching the application to their return.

Depending on their status and circumstance they may also be eligible to receive federal tax rebates and some other benefits under the tax law for themselves or their dependents. This includes the Child Tax Credit when a dependent child is a citizen or meets criteria in the IRS code. What resident aliens cannot collect is the Earned Income Tax Credit. It says so right on the ITIM application.

These IRS issued ITIN’s have be around at least since the 1960’s but some on the right what to use this rediscovered revelation to accuse President Obama of buying votes by making the IRS issues Child Tax Credits to “illegals.” This claim ignores the fact that all resident aliens are ineligible to vote. Some conservatives also want to pin on Obama their outrage that undocumented aliens are even allowed to report income without the threat of deportation. They would prefer, I suppose, that undocumented aliens be exempt from paying income tax, or else forced to hide their income out of fear of instant deportation.

Immigration enforcement is not the job of the IRS. It is their job to collect taxes on all residents who earn income regardless of whether they are citizens. It will be interesting to see if this issue gains traction or finds its way into round 2 of the immigration reform debate on the horizion.

The Real IRS Tax Scandal

by Brian T. Lynch, MSW

Here is the Internal Revenue Service controversy in a nut shell. Rank and file IRS agents used search terms such as “tea party” to triage a mountain of applications for tax exempt status. What the agents were trying to identify were applications where the purposes of the organizations were primarily political. Under IRS regulations, organizations applying for 501(c)(4) tax exempt status must primarily be involved in social welfare activity. All the triaged applications were eventually approved. Virtually everyone agrees the IRS must be politically neutral, so the methods the agents used to organize their workload is not an acceptable practice.

This principle and these core facts are not in dispute by anyone familiar with the details. The partisan contentions understandably arise from the lengthy inaction by senior IRS officials to end this practice. Were senior managers incredibly blind to what agents were doing or did they turn a blind eye? If it was the latter, did they ignore the practice for practical reasons or political reasons? Who up the political chain of command knew of the practice and when did they learn about it?

As happens often in today’s politically charged atmosphere, the partisan conflagration set off by the revelations is sucking all the oxygen out of the room leaving no one to explore why these practices developed in the first place. The “scandal” is a media induced distraction from much more serious problems under the surface. Among the questions we should be asking are these:

Is there an increase in tax exempt applications and is the increase asymmetrical?

Probably so, although the assessment of this is indirect. According to an analysis of data released by the IRS in response to the criticism, Martin A. Sullivan of TaxAnalysitst.org found that among the tax exempt applications approved by the IRS about two-thirds were submitted by conservative organizations. The remainder were either liberal leaning organizations or politically neutral. According to Professor Rob Reich in the April/May Boston Review, there has also been an unprecedented growth in the number of charitable foundation, or 501(c)(3) organizations. He attributes this to the growing wealth of the richest Americans. They are establishing foundations to leave a legacy and project their political influence on society from beyond the grave. So far, according to the IRS and other sources, there does appear to be a sharp increase in 501(c)(3) and (4) applications for tax exempt status. It also appears that this increase in applications are skewed towards conservative organizations and wealthy donors.

Is there a problem with tax exempt 501(c)(3) and (4) organizations being too overtly political, and if so, is the problem asymmetrical?

Image of Karl Rove by chicagopublicmedia/Flickr

According to some sources, since the Supreme Court’s Citizens United case there has been a growing number of wealthy people and corporations creating charitable foundations and social welfare organizations through which predominantly political messages are being delivered to the public, tax free. Just as we have increasingly been subsidizing big business through corporate welfare, we may now be subsidizing political messaging campaigns directed at us.

Here is an experiment readers can replicate for themselves. Type “left wing organizations” in a Google search. You will see that two right wing organizations and one left wing organization pop up. The first of these is discoverthenetwors.org, a “Guide to the Political Left” put out by David Horowitz’ Freedom Center Foundation. This guide is an alphabetical listing of allegedly left wing organizations, but looking down the list you will see it lumps together such “subversive” left wing organizations as the AARP and Abu Nidal. Abu Nidal is a Middle-East, “Spinoff of the Palestine Liberation Organization… [that] Has killed or maimed more than 900 people in over 20 countries.”

According to it’s mission, “The David Horowitz Freedom Center combats the efforts of the radical left and its Islamist allies to destroy American values and disarm this country as it attempts to defend itself in a time of terror.”

Painting the American left as affiliates of Islamist terrorists (or other notorious dictatorships as seen in on other sites) is a common theme on some conservative websites. This information is what passes as a public educational service justifying tax exempt status. Additionally, the site contains ads, which may or may not be paid advertizing. The site does claim to be 501(c)(3) tax exempt and solicits the viewers tax exempt donations.

The next organization on the search list is the Western Center for Journalism. It bills itself as a 501(c)3 tax exempt foundation and accepts tax exempt donations, yet it describes itself as a conservative organization and promotes a book written by the organizations current president, Floyd Brown. Brown’s latest book, “Obama Enemies List: How Barack Obama Intimidated America and Stole the Election”, was released in January 2013. Virtually all of the contents on this site are partisan in topic and perspective. One article by Steve Baldwin, for instance, starts out this way:

” Very few Americans realize there exists a large network of far left philanthropists and foundations in America dedicated to destroying the American way of life, our Christian-based culture and our free enterprise system. They seek to remove America from its constitutional foundations and move it toward a European-style socialism. Much of this effort is coordinated by a little known group called the Tides Foundation and its related group, the Tides Center.”

So I looked into the Tides Center and found it to be a 501(c)(3) organization dedicated to fund projects related to:

“ Art & Film, Civic Engagement, Civil Discourse, Community Development, Disability Rights, Economic Justice,’ Economic Opportunity, Education/Training, Environmental Sustainability, Faith & Spirituality, Food & Agriculture, Health Services/Healthcare Reform, HIV/AIDS, Housing/Homelessness, Human Rights, Immigration, International Development, LGBT Issues, Media ,Native Communities, Nonprofit Spaces, Peace & Conflict Resolution, Professional Development, Racial Justice, Reproductive Justice & Health, Technology, Women & Gender, Youth Development & Organizing”

Donations to the Tides Center are tax exempt, but other than its support for some issues unpopular with conservatives you will find nothing overtly political on the web site.

The third organization on the Google search list is the RightWingWatch.org operated by People for the American Way. This is a liberal organization. RightWingWatch was on the search list in connection with an article refuting a claim by Rick Joyner that Timothy McVeigh (Oklahoma City Bomber) was actually a left wing radical, not a right wing terrorist. Rick Joyner is the founder and executive director of MorningStar Ministries and Heritage International Ministries. He is also the Senior Pastor at the MorningStar Fellowship Church, a tax exempt organization.

People for the American Way bills itself as a 501(c)(4) organization, but they don’t use our tax money. When you donate you get this disclaimer:

“Because we lobby Congress, donations to People For the American Way, a nonprofit 501(c)(4) organization, are not tax deductible.”

In contrast, Freedom Works Foundation is a conservative non-profit organization. It is currently headed by former U.S. House Majority Leader Dick Armey, a Republican. The site say it is inspired by the leadership of Barry Goldwater and Ronald Reagan. It’s content is distinctly and exclusively conservative. If you press the icon to donate to the foundation web site you are taken to the donation page for Freedom Works (without the word “foundation”) which is a political action organization. There you will be given a choice to donate, “… where my donation will be used directly in the fight in Washington,” or “… where my donation will be 100% tax deductable and will be used for education, research and other efforts.” So the Freedom Works Foundation, which is tax exempt, shares the donation page of Freedom Works, which isn’t tax exempt.

Now, for symmetry sake, Google “right wing organizations.” The first three organizations (excluding the C.S. Monitor) on the search list are People for the American Way (or RightWingWatch), which does not count donations as tax deductions, the PublicEye.org operated by a tax exempt group named Political Research Associates, and Common Dreams, also tax exempt. The Common Dreams link is to a three paragraph article on the resignation of the IRS commissioner. It isn’t particularly political. The People for the American Way provides an extensive list of right leaning organizations with detailed information on each. Unlike the David Horowitz Freedom Center, this list appears to contain only US organizations. There is no attempt to link these groups to foreign or domestic terrorist organizations. The site describes their effort this way:

“Right Wing organizations come in all shapes and sizes, from think tanks to legal groups, local and national lobbying organizations, foundations and media forums. At any given moment, the Right is at work in our public school systems, courthouses, in Congress and state assemblies. At the same time, right-wing groups are reaching huge audiences through media outlets they own or influence — promoting regressive policies that seek to drive wedges between and among Americans.”

So regressive policies and promoting division among citizens is the worst this group has to say about right wing organizations.

Political Research Associates also provides a list of right wing organizations similar to the one at the PFAW. This list is far less detailed. It doesn’t include foreign or terrorist organizations. There are no militia groups, or hate groups or overtly raciest organizations on the list as far as I can tell. It doesn’t include the Aryan Nation or the Klu Klux Klan, for instance.

This isn’t an exhaustive survey, of course. It’s just an exercise. But on the face of things it does appear that some tax exempt organizations have a very political agenda. It also seems that conservative leaning non-profits are more overtly political and include more information of questionable educational value. The problem of political activity among tax exempt groups seems asymmetrical. The added value to the public worthy of extending tax credits to these, or to any overtly political organization is dubious.

Does the IRS have the personnel and resources to properly handle their workload?

According to the IRS, the answer is no. IRS funding was held flat for three years between FY 2005 and 2007. There was a 2.5% cut in its 2012 budget and now it is being squeezed by budget cuts and the sequestration, prompting protests by IRS personnel. There is also this summary of the IRS situation prior to the last two years of budget cuts:

The most serious problem facing U.S. taxpayers is the combination of the IRS’ expanding workload and the limited resources available to the IRS to handle it. Among the consequences:

• the IRS is unable to adequately meet the service needs of the taxpaying public. [it’s only funded at an 80% level for this service.]

• the IRS is unable to adequately detect and address noncompliance, requiring honest taxpayers to shoulder a disproportionately large share of the tax burden.

• the IRS is unable to maximize revenue collection, contributing to the federal budget deficit.

—National Taxpayer Advocate, 2011 Annual Report to Congress

So the answer to this question seems to be no. This gives credence to claims that IRS line staff were triaging tax exempt applications to better handle their workloads. It also suggests that the problem of the huge collection gap, between what is owed and what is paid, won’t be fixed anytime soon. It has been estimated by the IRS’s own computer analysis that there are about a million tax returns each year that appear to contain fraudulent information but are not audited. At a time when the federal government is starving for revenue the anti-tax sentiments in congress seem to extent to collection of legally due taxes, not just tax increases.

Finally, is IRS agents to determine the degree of political activity permitted by current IRS regulations an impossible job?

The answer to this last question is yes, it is absolutely impossible. In the increasingly polarized politics of today there are often disagrements on who is a liberal or a conservative. The two camps can’t even on a common set of facts for any given topic. How can the IRS possibly create a suitable metric for deciding which 501(c)(4) organizations have crossed the political line. Even more importantly, why is the IRS even trying to make room for political activity for tax exempt organizations? The clear intent of the law excludes the from any political activity at all. This is what tax payers should demand in exchange for the tax break these organization receive from us.

Here then is the real scandal. The IRS, one of the most fundamental agencies in government, is under staff and without resources by congressional design at a time when it faces massive fraud and abuse, growing anti-tax sentiments and a groundswell of people and organizations trying to claim tax exemptions for overtly political purposes. It is trying to police this latter situation with an unenforceable and illegal regulation that it has been saddled with for over 60 years. Why isn’t this the real IRS scandal?

Tax Breaks Cost US More Revenue than Medicare, Defense or Social Security

Tax breaks, also know as federal tax spending, includes things like mortgage deductions, child tax credits and lowered tax rates on capital gains. The CBO published a report today on what these deductions and tax breaks cost the federal government in annual revenues. The total amount is enormous. The top 10 most revenue syphoning tax cuts (there are more than 200 tax deductions in all) cost $900 billion. Tax spending is greater than budge expenditures for Medicare, Defense, or Social Security. It equals 1/17th of the US economy (or GDP). But taxbreaks or loopholes don’t show up anywhere in the federal budget, so the relative size of these hidden expenses are not usually apparent. They don’t often make it into the national dialogue when we talk about the budget. Below is the CBO report summary.

congressional budget office

supporting the congress since 1975

http://cbo.gov/publication/43768

The Distribution of Major Tax Expenditures in the Individual Income Tax System

report date: May 29, 2013

A number of exclusions, deductions, preferential rates, and credits in the federal tax system cause revenues to be much lower than they would be otherwise for any given structure of tax rates. Some of those provisions—in both the individual and corporate income tax systems—are termed “tax expenditures” because they resemble federal spending by providing financial assistance to specific activities, entities, or groups of people. Tax expenditures, like traditional forms of federal spending, contribute to the federal budget deficit; influence how people work, save, and invest; and affect the distribution of income.

This report examines how 10 of the largest tax expenditures in the individual income tax system in 2013 are distributed among households with different amounts of income. Those expenditures are grouped into four categories:

- Exclusions from taxable income—

- Employer-sponsored health insurance,

- Net pension contributions and earnings,

- Capital gains on assets transferred at death, and

- A portion of Social Security and Railroad Retirement benefits;

- Itemized deductions—

- Certain taxes paid to state and local governments,

- Mortgage interest payments, and

- Charitable contributions;

- Preferential tax rates on capital gains and dividends; and

- Tax credits—

- The earned income tax credit, and

- The child tax credit.

Some of the provisions of law that reduce the amount of taxable income under the individual income tax also decrease the amount of earnings subject to payroll taxes. The figures presented in this report are generally based on the reduction in payroll taxes as well as the reduction in income taxes, but some figures separate those two effects. (Provisions that reduce payroll tax receipts generally reduce future Social Security benefits as well; that effect is not analyzed in this report.)

How Do Tax Expenditures Affect the Federal Budget?

Although the 10 major tax expenditures listed here represent a small fraction of the more than 200 tax expenditures in the individual and corporate income tax systems, they will account for roughly two-thirds of the total budgetary effects of all tax expenditures in fiscal year 2013, CBO estimates. Together, those 10 tax expenditures are estimated to total more than $900 billion, or 5.7 percent of gross domestic product (GDP), in fiscal year 2013 and are projected to amount to nearly $12 trillion, or 5.4 percent of GDP, over the 2014–2023 period. In addition, tax credits to subsidize premiums for health insurance provided through new exchanges to be established under the Affordable Care Act will represent a new tax expenditure beginning in 2014, estimated to equal 0.4 percent of GDP over the 2014–2023 period.

How Are Tax Expenditures Distributed Among Households?

The 10 major tax expenditures considered here are distributed unevenly across the income scale. In calendar year 2013, more than half of the combined benefits of those tax expenditures will accrue to households with income in the highest quintile (or one-fifth) of the population (with 17 percent going to households in the top 1 percent of the population), CBO estimates. In contrast, 13 percent of those tax expenditures will accrue to households in the middle quintile, and only 8 percent will accrue to households in the lowest quintile (see the top panel of the figure below).

When measured relative to after-tax income, those 10 major tax expenditures are largest for the lowest and highest income quintiles. In calendar year 2013, CBO estimates, the combined benefits will equal nearly 12 percent of after-tax income for households in the lowest income quintile, more than 9 percent for households in the highest quintile, and less than 8 percent for households in the middle three quintiles (see the bottom panel of the figure above).

The distribution of tax expenditures across the income scale varies considerably among the different tax expenditures. For example, CBO estimates that more than 90 percent of the benefits of reduced tax rates on capital gains and dividends will accrue to households in the highest income quintile in 2013, with almost 70 percent going to households in the top percentile. Those benefits will equal 2 percent of after-tax income for the highest quintile and 5 percent of after-tax income for households in the top percentile. In contrast, about half of the benefits of the earned income tax credit will accrue to households in the lowest income quintile, equaling 6 percent of after-tax income for households in that group.

Tax credits that will provide assistance in paying premiums in health insurance exchanges are excluded from the distributional results presented here because they are not in effect in 2013. When those tax credits come into effect, they will appreciably increase tax expenditures for households in the lower and middle income quintiles. Individuals and families who have income between 100 percent and 400 percent of the federal poverty guidelines and who meet certain other requirements will be eligible for those credits.

How Do Tax Expenditure Estimates Differ From Revenue Estimates?

Estimates of tax expenditures are traditionally intended to measure the difference between households’ tax liabilities under present law and the tax liabilities they would have incurred if the provisions generating those tax expenditures were repealed but households’ behavior was unchanged. Such estimates do not represent the amount of revenues that would be raised if those provisions were eliminated, because the changes in incentives that would result from eliminating those provisions would lead households to modify their behavior in ways that would mute the impact on revenues. For example, if the preferential tax rates on capital gains realizations were eliminated, taxpayers would reduce the amount of capital gains they realized. Because the size of that tax expenditure is estimated on the basis of the gains that are projected to be realized with the preferential rates in place, the amount of additional revenues that would be received if those preferences were eliminated would be smaller than the reported tax expenditure.