Home » Posts tagged 'Benefits'

Tag Archives: Benefits

Civil Service Pensions – A Marker for What We’ve Lost

In New Jersey, as in many other states with conservative Republican Governors, the state civil service pension systems are under attack. A friend of mine, who has followed Governor Chris Christie’s rhetoric in the newspapers, commented about how reasonable this sounded since the system seems to be going broke. But the story of the pension system in New Jersey is more complicated that the current political sound bites. Let me tell you a true story about how civil service pensions came to be a target for public ridicule.

But things were changing in 1979 when I began my civil service career, even though I didn’t know it at the time. Big business had begun organizing politically and started spending big bucks on lobbying government for laws and regulations more favorable to business. Industry organizations were created to raise money and coordinate anti-union marketing campaigns. Ronald Reagan came into power in 1980 and set the tone for union bashing by crushing the air traffic controllers union. Private sector wages, which up to that time always rose in to proportion to increases in hourly GDP, were frozen and have remained frozen ever since. A fear campaign and actual business tactics based on globalization made jobs less secure. Private company pension systems were intentionally dismantled by big corporations to quarterly boost profits. Profit sharing arrangements took their place initially so workers had to invest in their company for their hope of retirement income. Then Wall Street saw all this money and wanted some action. They got congress to pass the IRA laws and all that pension money went to them.

Instead of real raises, businesses only offered cost of living adjustments, which keeps up with inflation but doesn’t share the extra wealth that the growing hourly GDP created for their employers. That extra wealth went to CEO’s and wealthy stockholders, beginning the cycle of great income disparity we have today. At the same time, Reagan cut the top marginal tax rate from 70% to 28%, a windfall for the rich and a huge loss of tax revenue that the rest of us had to bear.

So while the raises, salaries and benefits I received were always sub-par compared with the private sector during the first half of my career, declining private sector wages and benefits, rather than civil service raises or improved benefits, is the reason civil service looks so good today. In fact, civil service benefits have been steadily eroding for the last 15 years but this decline is slower than the collapse of private sector benefits. Civil service salaries also have barely budged in years and actually declined when you factor in inflation. But the assault on private sector salaries and benefits makes civil service look great by comparison only.

Know this, if corporate business interests had not conspired to suppress wages in America over the last 40 years the median income for a family of four today would be over $100,000/year. Instead it is shrinking and down to $51,000/year.

My point is that people in this country who work in the private sector have to fight back to regain a fair bite of the wealth they create for their employers. Workers need to re-organize and demand their fair share of our GDP. Rather than tearing away at civil servant pensions, people should be working to recreate what has been taken from them and use civil service as the framework and model to rebuild private sector retirement security.

There are particulars about why the pension system in New Jersey is in so much financial trouble. It isn’t because it is too generous. It is in trouble because when New Jersey was flush with money during Governor Christie Whitman’s (R) term she stopped making payments. She said she did this because the stock market was booming at that time. She said the pension system was way over-funded and didn’t need more cash. By the time she finished bankrupting the state with massive tax cuts and increased credit spending, Governor James Florio (D) didn’t have the revenue to pay into the state pension system during his entire term in office. This default model became a habit with subsequent Governors. Nothing, or only fractional amounts, were paid into the retirement system for the last 20 years. Governor Chris Christie (R) refused to put money into the system a few year back, when he had the money to pay, saying he didn’t want to put money into a broken system. This is crazy talk since it was the Executive branch that broke the system in the first place by doing exactly what he was doing.

The New Jersey State Pension system is, to a lesser extent, also in trouble because it has been abused for years by politicians bumping up the salaries of their political cronies just before retirement so they get huge pensions that they didn’t deserve or contribute towards. Politician’s take advantage of the way pensions are calculated to reward their buddies.

New Employment and Health Care Stats Refutes Obamacare Opponents

by Brian T. Lynch, MSW

The latest labor statistics and health care statistics refute the false claims being made against the Affordable Care Act (ACA) by Obamacare opponents. The claims and facts below are summarized from an excellent op/ed in Forbes magazine by Rick Ungar, which can be found here:

CLAIM: Obamacare will lead to a decline in full-time employment as employers reduce hours to below 30 per week to avoid providing health benefits.

FACT: Numbers just released by the Bureau of Labor Statistics (BLS), shows that part-time workers in the U.S. fell by 300,000 since the Affordable Care Act became law. This past year, the first full year of Obamacare health coverage, full-time employment grew by over 2 million. Part-time employment leaders who oppose Obamacare. Fewer cops, fewer teachers, fewer folks providing essential social services in the public sector all to make political point.

CLAIM: Millions of Americans are losing their individual health insurance policy due to Obamacare.

FACT: A new study by Lisa Clemans-Cope and Nathaniel Anderson of the Urban Institute found that prior to the Affordable Care Act the number of people kept their individual policy was very low with just 17 percent retaining coverage for more than two years.” The Urban Institute conducted a survey last December that asked 522 people between the ages of 18 and 64, “Did you receive a notice in the past few months from a health insurance company saying that your policy is cancelled or will no longer be offered at the end of 2013?” Only 18.6% said their plan was cancelled because it didn’t meet ACA coverage requirements, while the expected cancellation rate was 17% in the years prior to Obamacare. You can find the following bar graph and read more in Health Affairs.

The 18.6 percent who lost individual health insurance coverage due to the ACA requirements amounts to about 2.6 million people. According to the Urban Institute researchers over half of these folks will be eligible for coverage assistance. Still, roughly one million people will have to replace their cancelled policy with something that may cost them more. This isn’t good but it is less dramatic than what has been reported and most of these individuals would have been in the same boat prior to the ACA.

Facts matter – The Gallup-Healthways Well-Being Index was also just released. It reveals that 15.9 percent of American adults are now uninsured, down from 17.1 percent for the last three months of 2013. That translates roughly to 3 million to 4 million people getting coverage who did not have it before. The the number of Americans who still do not have health insurance coverage is on track to reach the lowest quarterly number since 2008.

There are currently 5 to 8 million people who can’t access Medicaid because their political leaders oppose Obamacare. That means the number of people being denied access to Medicaid expansion for political reasons is greater than the number who have signed up for Obamacare so far. The Rand Corporation recently analyzed 14 of the states with governors who oppose the Medicaid expansion and found their actions will deprive 3.6 million people of health coverage under Obamacare. These states will forgo $8.4 billion in federal funding. Moreover, their political opposition to Obamacare will cost these states $1 billion for programs that partially compensate medical providers who care for the indigent. (see Huffington Post: http://www.huffingtonpost.com/2013/06/03/medicaid-expansion_n_3367301.html).

Below is an excerpt and table of the uninsured by state that is taken from the Health Affairs Blog, which you can goto at: http://healthaffairs.org/blog/2014/01/30/opting-out-of-medicaid-expansion-the-health-and-financial-impacts/

Clearly, if the extreme efforts underway to by politicians to derail the Affordable Care Act was instead focused towards making it work, Obamacare would be wildly successful.

Examining the numbers. The number of uninsured people in states opting in and opting out of Medicaid expansion is displayed in Exhibit 1. Nationwide, 47,950,687 people were uninsured in 2012; the number of uninsured is expected to decrease by about 16 million after implementation of the ACA, leaving 32,202,633 uninsured. Nearly 8 million of these remaining uninsured would have gotten coverage had their state opted in. States opting in to Medicaid expansion will experience a decrease of 48.9 percent in their uninsured population versus an 18.1 percent decrease in opt-out states.

Exhibit 1: Uninsured Population by State, Pre- and Post-ACA

Here is a link to a website where you can check out state-by-state enrollments using an inter-active map: https://www.statereforum.org/tracking-health-coverage-enrollment-by-state?gclid=COCG7ffPob0CFYt9OgodPTQALQ

And this link is to an inter-active map showing the state-by-state status on Medicaid expansion: https://www.statereforum.org/Medicaid-Expansion-Decisions-Map?gclid=CJ_i4L3Rob0CFYuXOgod2RMA4g

Immigration Myths Hide the Benefits Says US Chamber of Commerce

From the US Chamber of Commerce: This ultra-conservative organization finally comes clean with a DATA DRIVEN VIEWPOINT support their position on immigration and how it benefits the US economically. http://www.scribd.com/doc/179652570/Immigration-Myths-and-Facts

Immigration Myths and Facts

Despite the numerous studies and carefully detailed economic reports outlining the positive effects of immigration, there is a great deal of misinformation about the impact of immigration. It is critical that policymakers and the public are educated about the facts behind these fallacies. [Says the US Chamber of Commerce]

Below I present the major points of their arguments. Please go to their website to read a detailed explanation for each of these points.

JOBS MYTH: Every job filled by an immigrant is a job that could be filled by an unemployed American.

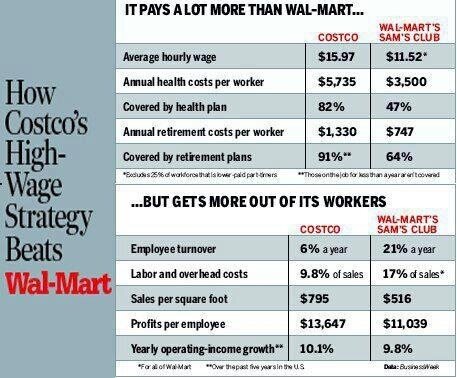

Higher Wages – Good for Families, Good for Economy & Good for Business

Below is another graphic that speaks for itself. Not only does paying higher wages improve the US economy and the lives of every citizen, it also makes good business sense.

I have written extensively on wage history and the case for a living wage, wealth distribution in America, our global business competitiveness, the dangers of our growing wealth inequality, and many other issues effecting middle and working class Americans, including and post on class warfare.

In a Labor Day message from former Secretary of Labor, Robert Reich, he, ” breaks down what it’ll take for workers to get a fair share in this economy — including big, profitable corporations like McDonald’s and Walmart to pony up and finally pay fair wages.

There is a petition that you can sign if you click on the above link. Please consider it your Labor Day obligation to those who struggled and even died to give you the benefits we still have today.

Time to Cap the Debate on Social Security and Medicare

Social Security and Medicare are in serious financial trouble in the future because they have been under attack for so long that how we thing of them has been changed by those who wish to kill these programs. Regardless of whose figures you believe when discussing the financial health of these programs, it could all be fixed by scraping the income cut off cap for contributions. Right now income payroll deduction collect a fixed percent of incomes up to around the first $107,000. This was just raised to this amount this year. All income over that amount is not considered.

I am a reluctant proponent of eliminating the Social Security and Medicare income contribution caps. In the short run this improve the income projects for both programs for some time to come, but it would also plant the seeds of distruction for these programs. It is helpful to understand why there are these caps to understanding my point.

Taxpayer Subsidized Downsizing in America

The business of quick and dirty layoffs has become a familiar feature in our culture. One recent example involved a journalist who worked at a large news organization. He was new to the company so he gratefully accepted the friendship of a well respected senior reporter. One Friday morning his mentor emailed him about a story idea and ended it by writing, “I’ll see you at the 10 AM meeting.” This prompted the following email exchange:

“What meeting? I didn’t get the email.”

“I’ll forward it do you.”

Then a short time later: “Forget the email. This meeting isn’t for you. Don’t come to this meeting!”

This is how the newsroom learned that day of the layoffs. Many senior journalists were let go along with a few younger reporters to avoid the appearance of age discrimination. As these “redundant” employees filed from the meeting they were handed garbage bags for their personal effects and accompanied to their desks by hired chaperones. It was all over in an hour.

Coolly calculated business decisions and pitiless firings toss employees off company books and onto government unemployment rolls somewhere in this country nearly every week. No notices, no outplacement services, no severance pay and no extended benefits are required. In many cases there is no effort to treat employees with the dignity or respect they deserve.

Apart from union contracts or employment agreements, American companies have no legal obligations to citizens being fired. They need not assume any responsibility for the impact it has on an employee, their family or their community. The only business costs of any significance are the premiums companies pay for government unemployment insurance. This easy, low cost ability to fire workers is called “workforce efficiency” and the U.S. is among the most efficient in the world. We ranks 12th out of 144 nations according to the study on global business competitiveness .

In most other advanced nations there are laws requiring companies to provide loyal employees with advanced layoff notices, severance pay and other benefits. These structural costs for downsizing may make businesses a little less competitive, but it brings significant benefits. It helps maintain a stable workforce and postpones government funded assistance to severed employees while they look for jobs. Requiring larger companies to provide mandatory severance benefits helps the nations absorb minor bumps in the economy without adding to problems by throwing people out of work at the first sigh of trouble. It also happens to be a humane way for citizens to treat one another.

Here in this country we treat our labor force as if it were a commodity to be bought and discarded at will. In the end, big business lets taxpayers foot most of the costs for unemployment benefits and supplemental welfare services for people out of work. At the same time the pro-business lobby pushes Congress for business tax breaks and budget cuts in the programs that help the workers they leave behind. Isn’t it time we stopped bowing to the pro-business lobby and stand up for the American worker?

A Flat Tax Payroll Deduction Might Save Social Security

DATA DRIVEN POINT OF VIEW: Don’t be fooled. Discussions about raising or lowering Federal Income Taxes has little to do with Social Security and Medicare, which are separately funded by payroll deductions. Is there a funding crisis for Social Security and Medicare? A long term problem, yes. A crisis, no. Can America continue to afford these programs given the number of baby boomer retirements? The answer is yes, of course we can. We are the wealthiest county on Earth. Nations with far less wealthier already provide their citizens with much more generous benefits. The reason we feel the funding punch is that the structure we’ve enacted to pay for federal insurance benefits is so regressive.

We could institute a flat tax for Social Security and Medicare. The table below shows what this might generate in premiums at the current 7.65% rate of payroll deductions. This plan would clearly generate more revenue than needed for current benefits. A flat payroll tax of significantly less than the current 7.65% would be all that is needed to fully fund Social Security and Medicare. It would reduce payroll taxes for the majority of Americans.

|

Payroll Taxes for Social Security and Medicare

|

||||

|

Total Income from Wages

|

Amount Currently Deducted

|

Contribution As a % of Income

|

Contribution if deductions were based on a flat tax

|

|

|

$1,000

|

$77

|

7.65%

|

$77

|

This Segment Represents 57 million households

|

|

$10,000

|

$765

|

7.65%

|

$765

|

|

|

$50,000

|

$3,825

|

7.65%

|

$3,825

|

|

|

$100,000

|

$7,650

|

7.65%

|

$7,650

|

|

|

$500,000

|

$8,423

|

1.68%

|

$38,250

|

|

|

$1,000,000

|

$8,423

|

0.84%

|

$76,500

|

There are at least 100,000 household in this segment

|

|

$10,000,000

|

$8,423

|

0.084%

|

$765,000

|

|

|

$50,000,000

|

$8,423

|

0.017%

|

$3,825,000

|

|

|

$100,000,000

|

$8,423

|

0.0084%

|

$7,650,000

|

|

|

$500,000,000

|

$8,423

|

0.0017%

|

$38,250,000

|

|

|

$1,000,000,000

|

$8,423

|

0.00084%

|

$76,500,000

|

|

|

$10,000,000,000

|

$8,423

|

0.000084%

|

$765,000,000

|

|

This table assumes that income from wages for the wealthy are at least $110,100, which is the income cap for 2012, and assumes they are not self-employed. Income from investments are not subject to payroll deductions. Employers pay an additional 7.65% in payroll taxes for their employees. The self employed also pay corresponding more in payroll taxes for their Social Security and Medicare benefits. Additional payroll deductions for unemployment and disability insurance may also apply in certain states and with certain individual.

These programs exist for everyone, and everyone should contribute according to their means. Those who are fortunate enough not to need the benefits still have a moral obligation to assure a minimal level of care to those less fortunate, and a social obligation to contributed to those who gave a lifetime of labor creating the fabulous wealth that the wealthy have accumulated.

Fiscal Cliff’s Specific Tax Breaks About to Expire

Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010

From Wikipedia, the free encyclopedia

Key aspects of the law include:

§ Extending the EGTRRA 2001 income tax rates for two years. Associated changes in itemized deduction and personal exemption rules are also continued for the same period. The total negative revenue impact of this was estimated at $186 billion.[7]

§ Extending the EGTRRA 2001 and JGTRRA 2003 dividends and capital gains rates for two years. The total negative revenue impact of this was estimated at $53 billion.[7]

§ Patching the Alternative Minimum Tax to ensure an additional 21 million households will not face a tax increase. This was done by increasing the exemption amount and making other targeted changes. The negative revenue impact of this measure was estimated at $136 billion.[7]

§ The above three measures are intended to provide relief to more than 100 million middle-class families and prevent an annual tax increase of over $2,000 for the typical family.[8]

§ A 13-month extension of federal unemployment benefits.[2][9] The cost of this measure was estimated at $56 billion.[7]

§ A temporary, one-year reduction in the FICA payroll tax. The normal employee rate of 6.2 percent is reduced to 4.2 percent. The rate for self-employed individuals is reduced from 12.4 percent to 10.4 percent.[9] The negative revenue impact of this measure was estimated at $111 billion.[7]

§ Extension of the Child Tax Credit refundability threshold established by EGTRRA, ARRA, and other measures.[7] According to the White House, this would benefit 10.5 million lower-income families with 18 million children.[2]

§ Extension of ARRA’s treatment of the Earned Income Tax Credit for two years.[7] According to the White House, this would benefit 6.5 million working parents with 15 million children.[2]

§ Extension of ARRA’s American opportunity tax credit for two years, including extension of income limits applied thereto.[7] According to the White House, this would benefit more than 8 million students and their families.[2]

§ The above three provisions, as well as some other similar ones, are intended to provide about $40 billion in tax relief for the hardest-hit families and students.[8]

§ An extension of the Small Business Jobs and Credit Act of 2010‘s “bonus depreciation” allowance through the end of 2011, and an increase in that amount from that act’s 50 percent to a full 100 percent. For the year of 2012, it returns to 50 percent.[9] The White House hopes the 100 percent expensing change will result in $50 billion in new investments, thus fueling job creation.[2]

§ An extension of Section 179 depreciation deduction maximum amounts and phase-out thresholds through 2012.[9]

§ Together, the above two business incentive measures were estimated to have a negative revenue impact of $21 billion.[7]

§ Various business tax credits for alternative fuels, such as the Volumetric Ethanol Excise Tax Credit, were also extended.[10] Others extended were credits for biodiesel and renewable diesel, refined coal, manufacture of energy-efficient homes, and properties featuring refueling for alternate vehicles.[9] Also finding an extension was the popular domestic Nonbusiness Energy Property Tax Credit, but with some limitations.[7]

§ Estate tax adjustment. EGTRRA had gradually reduced estate tax rates until there was none in 2010. After sunsetting, the Clinton-era rate of 55 percent with a $1 million exclusion was due to return for 2011. The compromise package sets for two years a rate of 35 percent with an exclusion amount of $5 million. The negative revenue impact of this provision was estimated at $68 billion.[7][11]

§ An extension of the 45G short line tax credit, also known as the Railroad Track Maintenance Tax Credit, through January 1, 2012. This credit had been in place since December 31, 2004 and allowed small railroad companies to deduct up to 50% of investments made in track repair and other qualifying infrastructure investments.[12]

2. ^ a b c d e f “Tax Cuts, Unemployment Insurance and Jobs”. The White House. Retrieved December 17, 2010.

7. ^ a b c d e f g h i j k “Tax Cut Extension Bill Wends Its Way to White House”. Accounting Today. December 17, 2010. Retrieved December 17, 2010.

8. ^ a b “Fact Sheet on the Framework Agreement on Middle Class Tax Cuts and Unemployment Insurance |”. The White House. December 7, 2010. Retrieved December 10, 2010.

9 ^ a b c d e Dupree, Jamie (December 9, 2010). “Tax Cuts Compromise Package Summary”. The Atlanta Journal-Constitution. Retrieved December 10, 2010.

Take the Labor Quiz

How much to you know about economic changes in America’s labor force over the last 30 years? Apart from the occasional new article on Labor Day, few of us give much thought to the extraordinary sacrifices that were required of prior generations in order to bring us the level of comfort and dignity so many of us enjoy today. But the blessing our grand parents and great grand parents fought so hard to bring us are beginning to disappear. America, once the leader in raising up the middle class, has fallen behind many other advanced nations.

An article entitled “The Speedup” in the July-August, 2011 edition of Mother Jones, written by Monika Bauerlein and Clara Jeffery, takes a look at this issue. I created a pop quiz based on some of the facts in the article. Take the quiz to see how well you are doing as an American worker. There are only 7 questions, so it won’t take long. The answers are below. If you score very high you should take the afternoon off, maybe.

1. What does the USA have in common with Papua New Guinea, Sierra Leone, Liberia, Samoa and Swaziland?

a. We all celebrate the Fourth of July

b. Like us, baseball is their national pass-time.

c. We are the only six nations on earth that don’t have mandatory paid maternity leave.

2. In the last 30 years, American worker productivity (which can be measured as the amount of work we accomplish per hour) has:

a. Declined by 75%

b. Increased by 140%

c. Increased by over 240%

3. Increased productivity means more company profits since the labor costs per item is lower. So, given your answer to question number 2 above, in the past 30 years the average overall wages in the US has:

a. Decreased by 20%

b. Increased by over 50%

c. Increased by only 16%

4. Over this same 30 year period, the average income of the top 1% of Americans:

a. Increased by 20%

b. Increased by 40%

c. Increased by over 80%

5. The number of hours everyone works in a given week is something that impacts our family life, and the nations GDP. Germany has the highest GDP in Europe. So how many more hours per year (actual time on the job) do American’s work compared to German workers?

a. We work 80 hours, or almost two weeks more per year.

b. We work 198 hours, or almost five weeks more per year.

c. We work 378 hours, or almost 10 weeks more per year.

6. In this current recession the GDP of every nation initially plunged, but no nation was hit harder than Japan. Japan’s GDP dropped twice as much as did ours. So when it comes to jobs lost, which nation has the worst unemployment rate?

a. Canada

b. Japan

c. USA

7. One last question. In 1950 nearly 35% of all wage or salary earners in America were in a union. What percentage of this group were union members as of last year?:

a. About 25%

b. Almost 20%

c. Less than 15%

If you answered each of the above question with option C you are well informed. Congratulations!

If you didn’t answer C to any of the questions, you really should read the article in Mother Jones.

In fact, we all need to be better informed so we can come together to restore a measure of economic justice in America. Here are a few additional details regarding each of the quiz questions:

1. Not only is the US only one of 6 countries that don’t have paid maternity leave, we are one of 16 nations that don’t require our workers to have time off each week. We are one of only 9 nations that don’t require businesses to offer a paid annual leave. Every one of our competitor nations provide this for their citizens.

2. While productivity has soared in the last 30 years by over 240%, the real value increase in the minimum wage since 1990 went up by just 21%. The increase in the cost of living rose 67% since 1990. Our output of goods and services in most sectors of the economy far outstrips the employment that most of these sectors create.

3. While income for the wealthiest 1% of American’s rapidly rises every year, the wealth owned by the rest of us actually declined slightly during the Regan years until about 1997. The increase since then is anemic compared to the enormous amount of wealth created by our great American labor force.

4. The rise in income among the wealthy, as large as it is, pales in compared to their rise in wealth. The top 20% of the wealthiest Americans today own almost 85% of everything leaving just 15% of the remaining wealth for the rest of us to share.

5. Not only do American’s rack up more time on the clock than our competitor nations (almost 10 weeks per year more than Germany) this doesn’t include the time we work off the clock. For example, half of us check emails on weekends and 46% of us even check work emails on days we are home sick.

6. Japan was hit twice as hard by the recession in terms of their drop in gross domestic product (GDP), yet our employment rate dropped more than twice their rate. Canada’s decline in GDP and employment initially mirrored our own (not quite as bad) but today their employment rate is higher than it was before the recession while we are worse off than all our competitor nations. Mean while, many American corporations are reporting record high profits.

7. The declining trend in union membership in America is in lock step with the decline of the middle class. The poor have faired even worse. Union workers today make about $10,000 more per year than non-union workers, yet the working public would rather trash unions than join one. The tensions between private sector employees and public sector workers is largely the result of envy by private sector workers who lost higher wages and many of their benefits when they lost their union.

How do you think we are doing as Americans? Most Labor Day articles remind us of the social battles and sacrifices prior generations have faced to bring a little dignity into our lives. We are doomed to repeat the mistakes of history if we don’t learn from them. I hope this quiz highlights where America may be headed and prompts you to consider what it will take to save the middle class. This is the real purpose for celebrating Labor, especially on Labor Day.

Note: First published in 2011, little has changed for the better since.