Home » Posts tagged 'business' (Page 2)

Tag Archives: business

Immigration Myths Hide the Benefits Says US Chamber of Commerce

From the US Chamber of Commerce: This ultra-conservative organization finally comes clean with a DATA DRIVEN VIEWPOINT support their position on immigration and how it benefits the US economically. http://www.scribd.com/doc/179652570/Immigration-Myths-and-Facts

Immigration Myths and Facts

Despite the numerous studies and carefully detailed economic reports outlining the positive effects of immigration, there is a great deal of misinformation about the impact of immigration. It is critical that policymakers and the public are educated about the facts behind these fallacies. [Says the US Chamber of Commerce]

Below I present the major points of their arguments. Please go to their website to read a detailed explanation for each of these points.

JOBS MYTH: Every job filled by an immigrant is a job that could be filled by an unemployed American.

Carbon, Climate and a Mirror to Our Future

by Brian T. Lynch, MSW

If you asked most forward thinking Americans to name a disruptive challenge we face today, global warming would be high on the list. Climate changing levels of carbon dioxide have been released into the air and the impacts on weather, on raising ocean levels and melting glacier are underway. The most socially responsible among us are already reducing their carbon footprint by recycling, buying more efficient cars, better insulating their homes, buying Energy Star appliances, using florescent or LED lighting. More and more people are also taking advantage of incentive programs to install rooftop solar or wind power generation systems.

The impact from these early pioneers of change is still quite small relative to the problem, but it is significant. So significant, in fact, that the industries which release carbon dioxide to produce the energy we buy are feeling threatened. After all, every time you replace an incandescent light bulb with an LED bulb you reduce their revenue.

Our power generation and distribution companies can adapt by getting into the LED lighting business for example, or they can maladapt by killing government regulations and initiatives to reduce carbon emissions. It appears they have chosen to do both. Some energy companies are investing in wind, solar or other renewable energy technologies while others are busy hatching plans to manipulate the democratic process in order to scuttle government incentives and regulations that threaten their bottom line.

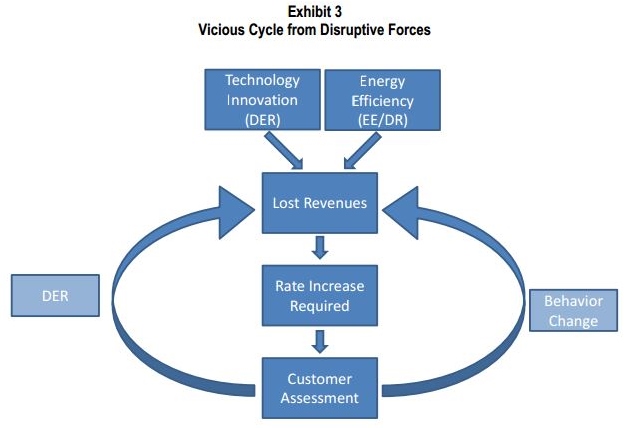

When the power generation utilities think about the disruptive challenges we face as a nation they quite literally see a mirror image of what the rest of us see. The threats they see include “demand side management” (DSM) which refers to consumer energy conservation measures, and “distributed energy resources” (DER) meaning residential power generation such as rooftop solar systems. This is explained in an national industry report released this past January by the Edison Electric Institute. Entitled, “Disruptive Challenges, Financial Implications and Strategic Responses to a Changing Retail Electric Business,” the report describes how disruptive consumer conservation and residential energy generation can be to their business. To help electric utility executives better understand the disruptive forces of socially responsible citizens it offers this useful flow chart: [http://tinyurl.com/m5py4rg]

Edison Electric Institute, Washington, D.C. – www.eei.org

Another study conducted for PacifCorp was released in March of 2013 by The Cadmus Group, Inc., another D.C. based firm. This industry study looks at the potential impact of consumer conservation on corporate energy sales over the next 20 years in states served by the Pacific Power and Rocky Mountain Power Companies. The Cadmus Group defined DSM this way:

Demand-side management involves reducing electricity use through activities or programs that promote electric energy efficiency or conservation, or more efficient management of electric energy loads. These efforts may:

- Promote high efficiency building practices

- Promote the purchase of energy-efficient ENERGY STAR® products

- Encourage the transition from incandescent lighting to more efficient compact fluorescent lighting

- Encourage customers to shift non-critical usage of electricity from high-use periods to after 7 p.m. or before 11 a.m.

- Consist of programs providing limited utility control of customer equipment such as air conditioners

- Promote energy awareness and education

This report suggests that energy conservation efforts and residential power generation over the next twenty years will reduce these energy company sales by up to 15%. About 76% of this reduction will come from residential customers, mostly from conservation measures. Numbers like these are causing energy companies everywhere to start defending their business model. The Arizona Public Service Company, for example, recently funded non-profit agencies to start what looks like a grass roots attempt to turn public opinion against both rooftop solar and the states’ publically elected Arizona Corporation Commission, which has final authority over utility rates. Rooftop solar initiatives are a prime target for utility companies both because of its rapid growth and the direct way these installations impact utility company profits. The reason why conservation efforts and residential power generation may be scary to utility companies from a business perspective becomes clear when you look at the bigger picture.

The history of U.S. energy use is one of annually increasing demand. Population growth and consumer purchases of more energy reliant products guarantee increased electric demand well into the future. It remains a growing market, but the rate of growth is slowing. This has been true since the 1950’s. According to the U.S. Energy Information Administration, “The growth of electricity demand (including retail sales and direct use) has slowed in each decade since the 1950s, from a 9.8-percent annual rate of growth from 1949 to 1959 to only 0.7 percent per year in the first decade of the 21st century.” The following chart shows how the increase in electric demand is declining in this country.

US. Energy Information Agency http://tinyurl.com/nnz9rgg

Meanwhile coal continues to be the biggest fuel source for power plants. The use of coal accounts for about 42% of the electricity we generate. Coal is expected to remain predominate though 2040, although its share of the energy generation mix will fall to around 35% of the total as natural gas and renewable energy soruces grow. This means that for the foreseeable future carbon emissions and growing electricity demand will still be with us if nothing changes. Of course nothing ever stays the same. The real question is whether the energy utilities, reacting to market forces, will dominate the direction we take in producing carbon based energy or whether pressure to save the planet will rise to a point where we can achieve meaningful reductions in green house gas emissions.

Higher Wages – Good for Families, Good for Economy & Good for Business

Below is another graphic that speaks for itself. Not only does paying higher wages improve the US economy and the lives of every citizen, it also makes good business sense.

I have written extensively on wage history and the case for a living wage, wealth distribution in America, our global business competitiveness, the dangers of our growing wealth inequality, and many other issues effecting middle and working class Americans, including and post on class warfare.

In a Labor Day message from former Secretary of Labor, Robert Reich, he, ” breaks down what it’ll take for workers to get a fair share in this economy — including big, profitable corporations like McDonald’s and Walmart to pony up and finally pay fair wages.

There is a petition that you can sign if you click on the above link. Please consider it your Labor Day obligation to those who struggled and even died to give you the benefits we still have today.

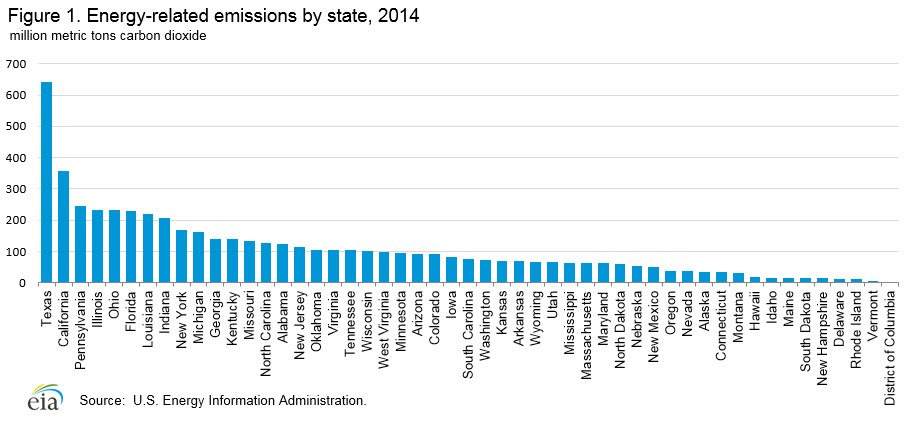

Texas, Where Carbon is King

Take one look at the state-by-state CO2 admission rates and it is immediately apparent that two states stand out from the rest, California and Texas. Of these two, Texas stands head and shoulders over California. Over the span of ten years Texas produced over 7.5 trillion metric tons of CO2, That is more than the 19 lowest emissions states plus D.C. combined. Amost 12% of al the CO2 emissions generated in the United States came from Texas. Californai produced 6.6% while Pensyulvania, Ohio, Florida and Illinois each produce between 4.6% and 4% of the nations CO2 emissions.

What are the implications for carbon conservation when more than one-sixth (18.3%) of all CO2 emissions are coming from just two states? For one thing it suggests that focusing national efforts on Texas and California can produce the biggest improvements in the short term. Furthermore, the data suggests that half the states with the lowest emissions are already working harder to reduce further carbon emissions that higher CO2 producing states. Among the higher CO2 producing states, Florida, Georga, Kentucky, Missouri, Oklahoma, Arizona, Colorodo and South Carolina increased their carbon polution between 2000 and 2010. Of these, the states with the highest rate of increase were Arazona (9.9%) and Colorado (11.8%). The largest state increase in carbon emissions over ten years was Nabraska (16.0%). So focusing our national effort on just a hand full of states might be the best strategy to make the biggest and quickest improvements in our carbon footprint in the world.

US ENERGY INFORMATION ADMINISTRATION

http://www.eia.gov/environment/emissions/state/analysis/

Release Date: May 13, 2013 | Next Release Date: May 2014 | full report State-Level Energy-Related Carbon Dioxide Emissions, 2000-2010

| Table 1. State energy-related carbon dioxide emissions by year (2000 – 2010) | ||||||||||||||

| million metric tons carbon dioxide | ||||||||||||||

| Change | ||||||||||||||

| 2000 to 2010 | ||||||||||||||

| State | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | Percent | Absolute | |

| District of Columbia | 4.3 | 4.1 | 4.2 | 3.9 | 4.0 | 3.9 | 3.2 | 3.4 | 3.1 | 3.2 | 3.3 | -23.6% | -1.0 | 40.6 |

| Vermont | 6.8 | 6.6 | 6.4 | 6.5 | 7.0 | 6.8 | 6.7 | 6.6 | 6.1 | 6.3 | 6.0 | -10.8% | -0.7 | 71.9 |

| Rhode Island | 11.6 | 12.1 | 11.6 | 11.3 | 10.8 | 11.0 | 10.4 | 11.0 | 10.6 | 11.3 | 11.0 | -4.8% | -0.6 | 122.6 |

| South Dakota | 14.1 | 13.4 | 13.7 | 13.6 | 13.7 | 13.2 | 13.3 | 13.9 | 15.1 | 14.9 | 15.1 | 7.3% | 1.0 | 154.1 |

| Delaware | 16.3 | 15.7 | 15.5 | 16.1 | 16.1 | 17.0 | 15.8 | 16.7 | 15.9 | 11.8 | 11.7 | -27.9% | -4.5 | 168.7 |

| Idaho | 15.6 | 15.5 | 14.9 | 14.2 | 15.5 | 15.7 | 15.8 | 16.3 | 15.8 | 15.4 | 16.2 | 4.0% | 0.6 | 170.9 |

| New Hampshire | 17.5 | 16.9 | 17.6 | 20.8 | 21.9 | 21.3 | 19.4 | 19.3 | 19.1 | 17.3 | 17.0 | -2.8% | -0.5 | 208.0 |

| Hawaii | 18.8 | 19.2 | 20.5 | 21.5 | 22.6 | 23.2 | 23.5 | 24.4 | 19.7 | 18.9 | 18.9 | 0.7% | 0.1 | 231.1 |

| Maine | 22.3 | 22.4 | 24.0 | 23.4 | 24.0 | 23.1 | 21.3 | 21.0 | 19.4 | 18.6 | 18.5 | -17.1% | -3.8 | 238.1 |

| Montana | 31.3 | 31.9 | 30.7 | 32.7 | 34.5 | 35.5 | 35.8 | 37.8 | 36.1 | 32.5 | 34.9 | 11.4% | 3.6 | 373.6 |

| Connecticut | 42.8 | 41.5 | 39.9 | 42.3 | 44.4 | 43.9 | 40.9 | 40.3 | 38.2 | 36.5 | 36.9 | -13.7% | -5.8 | 447.7 |

| Oregon | 41.2 | 40.6 | 39.1 | 39.3 | 40.6 | 41.0 | 40.3 | 43.8 | 43.2 | 41.2 | 40.3 | -2.4% | -1.0 | 450.6 |

| Nevada | 45.3 | 44.6 | 41.4 | 43.4 | 47.7 | 49.8 | 41.5 | 41.8 | 41.2 | 39.7 | 38.1 | -15.9% | -7.2 | 474.3 |

| Alaska | 44.3 | 43.4 | 43.6 | 43.5 | 46.8 | 48.1 | 45.8 | 44.1 | 39.5 | 37.9 | 38.7 | -12.6% | -5.6 | 475.6 |

| Nebraska | 41.4 | 42.7 | 42.2 | 43.0 | 43.1 | 43.5 | 44.1 | 44.5 | 46.5 | 46.8 | 48.0 | 16.0% | 6.6 | 485.7 |

| North Dakota | 50.8 | 51.7 | 51.4 | 50.9 | 49.5 | 52.4 | 50.8 | 52.6 | 53.1 | 51.4 | 52.5 | 3.3% | 1.7 | 567.1 |

| New Mexico | 58.0 | 58.2 | 55.2 | 57.3 | 58.5 | 59.1 | 59.9 | 59.1 | 57.6 | 58.5 | 54.8 | -5.5% | -3.2 | 636.2 |

| Arkansas | 63.2 | 62.4 | 60.9 | 61.3 | 61.9 | 59.7 | 61.6 | 63.1 | 63.7 | 61.6 | 66.1 | 4.6% | 2.9 | 685.8 |

| Wyoming | 62.7 | 63.0 | 61.7 | 63.4 | 63.4 | 62.8 | 63.7 | 66.1 | 66.8 | 63.7 | 64.9 | 3.5% | 2.2 | 702.3 |

| Mississippi | 60.6 | 69.4 | 61.9 | 63.2 | 64.8 | 63.2 | 65.4 | 67.7 | 64.1 | 60.4 | 65.5 | 8.0% | 4.9 | 706.1 |

| Utah | 65.1 | 62.9 | 62.1 | 62.7 | 65.3 | 67.0 | 68.3 | 70.4 | 69.9 | 65.0 | 64.2 | -1.3% | -0.9 | 723.0 |

| Kansas | 76.1 | 71.8 | 76.6 | 78.4 | 75.8 | 72.0 | 72.1 | 80.1 | 76.9 | 75.0 | 75.0 | -1.3% | -1.0 | 829.7 |

| Maryland | 77.5 | 78.0 | 77.9 | 80.4 | 82.0 | 83.9 | 77.5 | 78.1 | 74.7 | 71.4 | 70.5 | -9.0% | -7.0 | 852.0 |

| Washington | 82.8 | 79.4 | 72.8 | 74.5 | 76.7 | 78.3 | 76.3 | 81.8 | 79.6 | 77.5 | 76.1 | -8.1% | -6.7 | 855.9 |

| Massachusetts | 82.2 | 82.1 | 82.9 | 83.8 | 82.6 | 84.3 | 76.4 | 80.0 | 77.2 | 71.0 | 73.0 | -11.2% | -9.2 | 875.6 |

| Iowa | 77.7 | 76.6 | 77.2 | 76.4 | 78.9 | 78.9 | 80.2 | 85.7 | 88.3 | 83.8 | 88.7 | 14.1% | 11.0 | 892.4 |

| South Carolina | 79.3 | 78.0 | 79.2 | 79.5 | 87.1 | 85.7 | 86.4 | 87.0 | 85.5 | 80.7 | 84.0 | 5.9% | 4.7 | 912.5 |

| Colorado | 84.7 | 92.8 | 90.9 | 90.0 | 93.1 | 95.4 | 96.4 | 99.2 | 97.6 | 93.7 | 96.5 | 13.9% | 11.8 | 1,030.3 |

| Arizona | 86.0 | 88.3 | 87.7 | 89.3 | 96.6 | 96.7 | 100.0 | 102.2 | 103.1 | 94.6 | 95.9 | 11.6% | 9.9 | 1,040.5 |

| Minnesota | 97.7 | 94.7 | 97.3 | 101.0 | 100.6 | 101.7 | 99.1 | 100.9 | 100.6 | 93.1 | 93.4 | -4.4% | -4.3 | 1,080.3 |

| Wisconsin | 107.5 | 105.5 | 106.7 | 104.3 | 107.1 | 110.5 | 102.7 | 104.7 | 105.7 | 96.7 | 99.2 | -7.7% | -8.3 | 1,150.6 |

| Oklahoma | 100.1 | 101.4 | 101.6 | 103.5 | 99.8 | 106.9 | 110.2 | 109.6 | 113.1 | 104.9 | 103.4 | 3.4% | 3.4 | 1,154.5 |

| West Virginia | 113.4 | 103.5 | 116.2 | 112.5 | 109.8 | 111.9 | 112.2 | 114.6 | 110.6 | 89.1 | 98.9 | -12.7% | -14.4 | 1,192.8 |

| Virginia | 122.3 | 120.0 | 118.5 | 122.2 | 126.5 | 128.5 | 122.0 | 127.7 | 117.4 | 106.3 | 109.8 | -10.2% | -12.5 | 1,321.3 |

| Tennessee | 125.2 | 124.2 | 123.2 | 120.9 | 123.0 | 124.6 | 127.0 | 126.7 | 120.3 | 100.3 | 107.1 | -14.5% | -18.1 | 1,322.4 |

| New Jersey | 121.1 | 118.5 | 118.9 | 119.8 | 122.6 | 127.6 | 120.2 | 128.6 | 124.3 | 110.4 | 115.4 | -4.7% | -5.7 | 1,327.5 |

| Missouri | 125.4 | 131.1 | 131.8 | 138.3 | 140.0 | 143.0 | 141.6 | 140.8 | 137.9 | 131.6 | 135.7 | 8.2% | 10.3 | 1,497.2 |

| Alabama | 140.4 | 132.0 | 136.7 | 137.2 | 139.7 | 141.5 | 144.0 | 146.1 | 139.2 | 119.8 | 132.7 | -5.5% | -7.7 | 1,509.3 |

| North Carolina | 147.7 | 143.1 | 144.3 | 144.7 | 148.2 | 152.7 | 147.4 | 153.6 | 149.0 | 132.9 | 142.9 | -3.3% | -4.8 | 1,606.4 |

| Kentucky | 144.7 | 148.1 | 148.3 | 143.9 | 150.9 | 153.2 | 156.1 | 156.4 | 153.7 | 143.7 | 150.7 | 4.2% | 6.1 | 1,649.7 |

| Georgia | 167.9 | 160.3 | 165.1 | 167.5 | 173.3 | 183.9 | 181.5 | 184.6 | 173.5 | 163.4 | 173.7 | 3.4% | 5.8 | 1,894.7 |

| Michigan | 192.6 | 188.5 | 187.9 | 184.7 | 187.4 | 189.3 | 178.2 | 181.2 | 175.2 | 164.4 | 165.9 | -13.9% | -26.7 | 1,995.1 |

| New York | 211.4 | 206.7 | 200.8 | 210.1 | 213.9 | 210.7 | 192.5 | 199.4 | 190.5 | 175.5 | 172.8 | -18.3% | -38.6 | 2,184.4 |

| Louisiana | 239.9 | 211.9 | 219.8 | 214.6 | 226.2 | 221.7 | 236.0 | 234.5 | 221.7 | 203.9 | 223.5 | -6.8% | -16.4 | 2,453.6 |

| Indiana | 238.2 | 228.6 | 231.7 | 236.9 | 237.8 | 236.7 | 235.0 | 234.7 | 231.5 | 208.5 | 219.1 | -8.0% | -19.1 | 2,538.6 |

| Illinois | 232.1 | 223.1 | 225.1 | 227.7 | 235.2 | 242.0 | 233.9 | 242.1 | 240.7 | 226.1 | 230.4 | -0.7% | -1.7 | 2,558.3 |

| Florida | 239.2 | 238.1 | 241.3 | 244.9 | 257.3 | 260.9 | 259.5 | 257.8 | 240.2 | 226.3 | 246.0 | 2.8% | 6.7 | 2,711.7 |

| Ohio | 264.0 | 254.5 | 260.3 | 267.4 | 262.5 | 269.7 | 263.0 | 268.9 | 261.9 | 237.6 | 249.1 | -5.6% | -14.9 | 2,858.9 |

| Pennsylvania | 276.3 | 263.4 | 270.1 | 273.0 | 276.6 | 280.0 | 274.1 | 277.6 | 264.9 | 246.0 | 256.6 | -7.1% | -19.7 | 2,958.7 |

| California | 381.3 | 385.8 | 384.9 | 389.5 | 391.5 | 389.0 | 397.5 | 403.7 | 389.8 | 375.9 | 369.8 | -3.0% | -11.4 | 4,258.6 |

| Texas | 711.3 | 704.1 | 715.8 | 706.4 | 709.7 | 677.8 | 675.2 | 676.7 | 653.3 | 624.9 | 652.6 | -8.3% | -58.8 | 7,507.7 |

| Total1 | 5,879.9 | 5,772.4 | 5,810.0 | 5,857.5 | 5,968.8 | 6,000.4 | 5,921.6 | 6,029.0 | 5,842.9 | 5,441.8 | 5,631.3 | -4.2% | -248.6 | 64,155.6 |

| 1For the United States as a country see, EIA, Monthly Energy Review, Section 12: Environment. Differing methodologies between the two data series causes | ||||||||||||||

| the total for all states to be slightly different from the national-level estimate. The amount varies no more than 0.5 percent. See Appendix A for details on | ||||||||||||||

| the data series differences. | ||||||||||||||

| Source: U.S. Energy Information Administration (EIA), State Energy Data System and EIA calculations made for this analysis. | ||||||||||||||

| Note: The District of Columbia is included in the data tables, but not in the analysis as it is not a state. | ||||||||||||||

See How Much Money it Takes to Be Financially Secure in Your Town

What follows is a Family Budge Calculator put out by the Economic Policy Institute. www.epi.org/resources/budget/ The example shown here is for a two parent family with two children living in the capital city of New Jersey, Trenton. A typical family there needs over $75,000 in income per year to be financially secure. That means each parent would have to work full-time and be making at least $18/hour. Or, if only one parent worked, they would need to be pulling in $36/hour for their family to be financially secure. This is a long ways from minimum wage.

Family Budget Calculator

EPI’s Family Budget Calculator measures the income a family needs in order to attain a secure yet modest living standard by estimating community-specific costs of housing, food, child care, transportation, health care, other necessities, and taxes. The budgets, updated for 2013, are calculated for 615 U.S. communities and six family types (either one or two parents with one, two, or three children).

As compared with official poverty thresholds such as the federal poverty line and Supplemental Poverty Measure, EPI’s family budgets offer a higher degree of geographic customization and provide a more accurate measure of economic security. In all cases, they show families need more than twice the amount of the federal poverty line to get by. [To see and use the actual calculator for yourself readers of WordPress must go to the website at http://www.epi.org/resources/budget/ ]

Family Types include:

One Parent, One Child One Parent, Two Children One Parent, Three Children Two Parents, One Child Two Parents, Two Children Two Parents, Three Children

States Include:

AK AL AR AZ CA CO CT DC DE FL GA HI IA ID IL IN KS KY LA MA MD ME MI MN MO MS MT NC ND NE NH NJ NM NV NY OH OK OR PA RI SC SD TN TX UT VA VT WA WI WV WY

Area Names In New Jersey Include:

Atlantic City, NJ MSA Bergen-Passaic, NJ HUD Metro FMR Area Jersey City, NJ HUD Metro FMR Area Middlesex-Somerset-Hunterdon, NJ HUD Metro FMR Area Monmouth-Ocean, NJ HUD Metro FMR Area Newark, NJ HUD Metro FMR Area Ocean City, NJ MSA Philadelphia-Camden-Wilmington, PA-NJ-DE-MD MSA Trenton-Ewing, NJ MSA Vineland-Millville-Bridgeton, NJ MSA Warren County, NJ HUD Metro FMR Area

RESULTS FOR TRENTON, NJ

Trenton-Ewing, NJ MSA (NJ)

Two Parents, Two Children

|

Item |

Cost |

|

Monthly Housing |

$1206 |

|

Monthly Food |

$754 |

|

Monthly Child Care |

$1258 |

|

Monthly Transportation |

$607 |

|

Monthly Health Care |

$1519 |

|

Monthly Other Necessities |

$502 |

|

Monthly Taxes |

$447 |

|

Monthly Total |

$6292 |

|

Annual Total |

$75508 |

Family budgets are for 2013.

Learn more about EPI’s Family Budget Calculator

OVERVIEW: What Families Need to Get By: The 2013 Update of EPI’s Family Budget Calculator (EPI Issue Brief #368)

METHODOLOGY: Economic Policy Institute 2013 Family Budget Calculator: Technical Documentation (EPI Working Paper #297)

DATA: Download source data (Excel)

Lobbying Produced a 22,000% Return for Corporations per One Study

Is lobbying Congress a good investment?

This is normally a nearly impossible question to answer, but a unique set of circumstances allowed researchers to conclude that Corporate lobbying for a tax amnesty provision in the 2004 American Jobs Creation Act(AJCA) yielded a 22,000% return. Yea, I would say it was worth it.

One reason why the question can’t normally be answered is that the financial information needed to answer the question can almost only be found on Corporate tax returns. All tax returns are confidential and only the IRS can see them. But a unique opportunity to study this question presented itself through a tax amnesty provision in the AJCA.

The University of Kansas School of Business ceased the opportunity. Researchers found that they were able, in this unique situation, to publicly obtain all the information need to analyze the return on lobbying expenditures. As stated in this study, “This is the first study to provide actual values of the financial savings arising from tax law changes, and the first to use data that has been audited by independent accounting firms.”

Cudos to the authors, Alexander, Mazza and Scholtz, and to the University of Kansas School of Business for this important piece of research.

Measuring Rates of Return for Lobbying Expenditures: An Empirical Analysis under the American Jobs Creation Act

Raquel Meyer Alexander

University of Kansas – School of Business

Stephen W. Mazza

University of Kansas – School of Law

Susan Scholz

University of Kansas – Accounting and Information Systems Area

April 8, 2009

Abstract:

The lobbying industry has experienced exponential growth within the past decade. The general public, the media, and special interest groups perceive lobbying to be a powerful mechanism affecting public policy. However, academic research finds inconclusive results when quantifying the rate of return on political lobbying expenditures. In this paper we use audited corporate tax disclosures relating to a tax holiday on repatriated earnings created by the American Jobs Creation Act of 2004 to examine the return on lobbying. We find firms lobbying for this provision have a return in excess of $220 for every $1 spent on lobbying, or 22,000%. Repatriating firms are more profitable overall, but surprisingly, profitability is not a predictor of repatriation amount. Rather, industry and firm size are most predictive of repatriation. Cash on hand, a proxy for ability to repatriate, is not associated with the repatriation decision or the repatriation amount. This paper provides compelling evidence that lobbying expenditures have a positive and significant return on investment.

Working Paper Series

GO TO THE WEBSITE AND DOWNLOAD THE FULL REPORT HERE http://bit.ly/Abj1Or

From the report:

|

[Top 20] Companies Repatriating $500M or More

(105 companies total1)

|

||||

|

Amount

|

Amount Repatriated/

|

|||

|

Rank

|

Company

|

Repatriated

|

Total Assets2

|

Revenue2

|

|

1

|

PFIZER

|

37,000

|

30%

|

70%

|

|

2

|

MERCK & CO

|

15,900

|

37%

|

68%

|

|

3

|

HEWLETT PACKARD

|

14,500

|

19%

|

18%

|

|

4

|

JOHNSON & JOHNSON

|

10,800

|

20%

|

23%

|

|

5

|

IBM

|

9,500

|

9%

|

10%

|

|

6

|

SCHERING-PLOUGH

|

9,400

|

59%

|

114%

|

|

7

|

DU PONT

|

9,100

|

26%

|

33%

|

|

8

|

BRISTOL-MYERS SQUIBB

|

9,000

|

30%

|

46%

|

|

9

|

ELI LILLY & CO

|

8,000

|

32%

|

58%

|

|

10

|

PEPSICO

|

7,500

|

27%

|

26%

|

|

11

|

PROCTOR & GAMBLE

|

7,200

|

13%

|

14%

|

|

12

|

INTEL

|

6,200

|

13%

|

18%

|

|

13

|

COCA-COLA

|

6,100

|

19%

|

28%

|

|

14

|

ALTRIA GROUP

|

6,000

|

6%

|

9%

|

|

15

|

MOTOROLA

|

4,600

|

15%

|

15%

|

|

16

|

DELL

|

4,100

|

18%

|

8%

|

|

17

|

MORGAN STANLEY

|

4,000

|

1%

|

10%

|

|

18

|

CITIGROUP

|

3,200

|

0%

|

3%

|

|

19

|

ORACLE

|

3,100

|

15%

|

26%

|

|

19

|

WYETH

|

3,100

|

9%

|

18%

|

GOP Doubles Down with Cynical Student Loan Bill

THE HOUSE HAS PASSED STUDENT LOAN SOLUTIONS, TIME FOR THE SENATE TO ACT

Posted by Nick Marcelli on June 18, 2013

Today, House Republican Leadership held a press conference to discuss the steps the House has taken to avoid the doubling of student loan rates on July 1. The House has already passed a solution to avoid the doubling of student loan rates that echoes the President’s own plan. It is time for the Senate to act.

BUT WAIT!

Take a closer look at what the GOP and Eric Cantor are touting as a positive step to help students pay for college.

Stafford Loan – Current fixed rate for this student loan is 3.4% and it is scheduled to double in July to 6.8%. The House GOP just passed the Smarter Solutions for Students Act (SSSA) which would end the fixed rate and calculate a variable rate at 2.5% points over the 10 year Treasury Bill rates, with a cap of 8.5% on Stafford Loans. The average 10 yr T bill rate so far this month is 2.66%, so the current Stafford Loan rate would be 5.16%.

While the 5.16% today is better than the 6.8% rate beginning in a few weeks, the variable rate cap of 8.5% is 1.7% higher than the fixed rate would be. So Congratulations to the House GOP for passing a plan that would both lower and raise student loan rates at the same time. If this isn’t cynical enough for you, add the SSSA’s current student loan rate of 5.16% today with the cap rate of 8.5% and then divide by two. This gives us the variable rates mid-range of 6.83%, nearly identical to the higher fixed rate as of July. So for bankers this is a revenue neutral proposal over a range of years while current college students get only a 52% rate increase as of July. For future college students the rate can more than double the current 3.4% fixed rate.

A look at the other provisions of the bill reveal similar findings. This could be a bill written by the student loan industry to squeeze more out of students without appearing to be quite as greedy.

Below is an analysis that (also cynically) does not assess the financial impact if the current 3.4% rate is allowed to stay the same.

H.R. 1911, Smarter Solutions for Students Act

cost estimate

may 20, 2013

read complete document (pdf, 28 kb)

As ordered reported by the House Committee on Education and the Workforce on May 16, 2013

H.R. 1911 would change the interest rates for all new federal loans to students and parents made on or after July 1, 2013, from a fixed interest rate set in statute to a variable interest rate, adjusted annually. Under the bill, interest rates for all new subsidized and unsubsidized student loans would be based on the interest rate on a 10-year Treasury note plus 2.5 percentage points, with a cap of 8.5 percent. (Borrowers pay no interest on subsidized loans while enrolled in school or during other deferment periods but are responsible for interest at all times on unsubsidized loans.) The interest rate for all new GradPLUS and parent loans would be based on the interest rate on a 10-year Treasury note plus 4.5 percentage points, with a cap of 10.5 percent. The bill also would eliminate the cap on the interest rate on all new consolidation loans (multiple loans for a single borrower combined into one loan) originated on or after July 1, 2013.

Under current law, all subsidized and unsubsidized loans originated on or after July 1, 2013, will have a fixed interest rate of 6.8 percent, and all GradPLUS and parent loans will have a fixed rate of 7.9 percent. In addition, the interest rate on all consolidation loans is capped at 8.25 percent.

CBO estimates that enacting H.R. 1911 would reduce direct spending by about $1.0 billion over the 2013-2018 period and by $3.7 billion over the 2013-2023 period. Enacting the bill would not affect revenues. Pay-as-you-go procedures apply because enacting the legislation would affect direct spending. Implementing the bill would not have a significant impact on spending subject to appropriation.

1st Qrt Report: Wages Sharply Down, Bank Profit at Record High

This is an mportant story that I want to share with readers of this blog. I encourage everyone to watch the video. Feel free to add your comments.

The Real News Network

Bank Profits Soar, Wages Suffer Sharpest Decline in 60 Years

Bill Black: The economy is recovering – unless you work for a paycheck. – June 9, 2013

JAISAL NOOR, TRNN PRODUCER: Welcome to The Real News Network. I’m Jaisal Noor in Baltimore. And welcome to the latest edition of The Black Financial and Fraud Report with Bill Black, who now joins us from Kansas City, Missouri. Bill is an associate professor of economics and law at the University of Missouri-Kansas City. He’s a white-collar criminologist and former financial regulator. And he’s the author of the book The Best Way to Rob a Bank Is to Own One.

Thank you for joining us, Bill.

BILL BLACK, ASSOC. PROF. ECONOMICS AND LAW, UMKC: Thank you.

NOOR: So, Bill, what can you tell us about this latest news from the first-quarter? Bank profits soared to record levels while wages suffered their sharpest decline since 1947.

BLACK: What it all adds up to, of course: it is a very good time and a very good country to be a plutocrat, because the rich are getting richer at a staggering rate and poor people are actually getting poorer, just like the same saying goes.

So we’ve got a series of news that it has just come in this week. One thing shows that we have the largest decline in wages. Boy, that’s a big win. And that follows–that’s for the first quarter of 2013. And that follows what was a huge quarter for income in the fourth quarter, in other words the last three months of 2012. But, of course, there’s a footnote on that. And that huge quarter at the end of last year was to beat the tax increase. So that was the massive payment of bonuses to the wealthiest Americans. So they made sure the wealthiest Americans got their money before the tax increases kicked in.

And what happened as soon as we got back to the regular economy? Well, wages haven’t simply stalled; they’ve actually gotten negative. And productivity is up, which is supposed to mean that wages are up, but wages have gone in the opposite direction. So that’s the news on the wages front.

On the bank profit front, hey, we’ve got the highest reported profits ever for the first quarter of this year. Now, the twist in all of this is that the statistics, when you look at them closely, show the banks weren’t all that profitable in their regular operations, because, of course, they’re not making all that much in the way of loans and such. They’re mostly sitting on their money.

So how did the banks report record profits, but when they were doing their day-to-day business they weren’t earning all that much in the way of super profits? And the answer to all of that is that they reversed out a whole bunch of reserves for future losses, which is the same game they played leading up to the crisis. So reserves for those massive future losses, they’ve made them lower and lower. At the end of 2006, they had gotten to the lowest level of reserves against future losses in history since the savings and loan debacle. And we all know how disastrously this ended. Well, guess what? We’re at the record low again in 2007.

And this is how the accounting works. Every dollar they take out of reserves for future losses is an additional dollar they can pay in bonuses to the top executives. So the wealthier are getting wealthier at a record rate in banking as well.

So what else is happening? Well, we have record stock market appreciation. In fact, there’s a neat headline that says that when you disregard inflation–which of course you can’t–the losses that people suffered in the Great Recession have now been made back. It took a lot of years to do it, but they’ve made it back. But, of course, there’s a footnote, and the footnote says this: well, regular people haven’t, but people who own stock have made out like bandits. They’ve had a recovery measured by $1.5 trillion, and 80 percent of that gain goes to the 20 percent of richest Americans. So, hey, stock market–great news for the wealthy.

Well, but there was also some potential good news. So housing prices have finally started to go upwards. And that’s good news for all kinds of Americans who own their homes. But, again, there’s a little hitch in all of this, ’cause it turns out that for the first time in American history, a huge portion of these gains are going to massive corporations and investment firms and hedge fund types, and they are because they’re making massive purchases of homes at distressed prices to serve as what we call in the trade vulture funds and to sell it back to regular folks when those housing prices have appreciated. So a lot of this gain in housing prices is not going to regular people; it’s going to go to the hedge fund executives, who are already the wealthiest people in the world.

And how does all of this sum it up? Well, I did a paper recently on the Nobel Prize awarded to Mr. Myerson. Dr. Myerson got this award in 2007 when the world was blowing up, and he got the award for proving that fraud couldn’t exist in the financial sector. And he proved this by assuming that fraud couldn’t exist. And his mechanism for assuming that fraud doesn’t exist is plutocracy. And indeed he says the great advantage of the market system compared to socialism is that we have billionaires, and he says that people who are not that rich, in other words, ordinary multimillionaires who are CEOs, if they act rationally–that’s his word–will loot their corporations. And so the only safe thing we can do is to make some segment of Americans billionaires–in fact, probably multibillionaires–so they can run our largest corporations and made–be made into mega-billionaires. So you get a Nobel Prize for creating a system that leads to recurrent intensifying financial crises that caused $10 billion in losses in the United States and the loss of $10 million jobs. And we are told that we’re supposed to be happy and bless the system because it creates plutocrats who have incomes in the multibillion dollars who, when there is a crisis–in the words of Myerson in another article, people who are poor should pay taxes to bail out billionaire bankers, because that will be good for the poor people. That’s the status of economics in the modern era.

NOOR: So, Bill, it would seem like the dominoes are in a row for another massive financial meltdown. Would you disagree?

BLACK: No, that’s exactly what they’re putting in place. And they’re going to make the folks wealthy on both ends, right? We’re told that they have to be made billionaires so that they can invest prudently during the expansion phase of the bubble. And as soon as they destroy the economy, we’re told that we have to bail them out and make them ever wealthier. And the way we do all of these things increases the rewards to fraud and reduces the penalty to fraud, and especially in the modern era where you can dilute with impunity under the administration’s too-big-to-prosecute-or-even-indict standard.

NOOR: And finally, Bill, where are the movements that are challenging these policies?

BLACK: Well, they’re certainly not in either of the major parties. There are, of course, progressives within the Democratic Party, and they do some things, but in truth, both parties’ leadership are heavily dependent on funding from the largest banks and from other plutocrats. You’ve just seen the the Obama administration put a Pritzker in a cabinet position where the Pritzkers have a terrible reputation. And you saw that the Republicans, who usually block anyone that Obama nominates, were more than happy to have one of those wealthy folks, who is one of their kind, in a cabinet position.

So the dissent remains on places that are not typically found in the mainstream media, the Occupy movements and such. And, you know, it’s going to be the next crisis before there’s any serious chance of serious reform.

NOOR: Thank you for joining us, Bill.

BLACK: Thank you.

NOOR: And thank you for joining us on The Real News Network.

Bio – William K. Black, author of THE BEST WAY TO ROB A BANK IS TO OWN ONE, teaches economics and law at the University of Missouri Kansas City (UMKC). He was the Executive Director of the Institute for Fraud Prevention from 2005-2007. He has taught previously at the LBJ School of Public Affairs at the University of Texas at Austin and at Santa Clara University, where he was also the distinguished scholar in residence for insurance law and a visiting scholar at the Markkula Center for Applied Ethics. Black was litigation director of the Federal Home Loan Bank Board, deputy director of the FSLIC, SVP and general counsel of the Federal Home Loan Bank of San Francisco, and senior deputy chief counsel, Office of Thrift Supervision. He was deputy director of the National Commission on Financial Institution Reform, Recovery and Enforcement. Black developed the concept of “control fraud” frauds in which the CEO or head of state uses the entity as a “weapon.” Control frauds cause greater financial losses than all other forms of property crime combined. He recently helped the World Bank develop anti-corruption initiatives and served as an expert for OFHEO in its enforcement action against Fannie Mae’s former senior management.

Market Logic’s Irrational Origin

In a side comment by Tim Worstall in his recent Forbes commentary, he says: “… if the social costs of climate change were clearly and obviously larger than the consumer benefits of CO2 emissions then we wouldn’t actually have a problem with climate change at all.” He says people would see the soical costs and stop using fossil fules.

That’s like saying smokers would stop smoking if they believed their collective habit raised national health care costs and caused premature death among their cohorts. People still smoke who believe this because human behavior is not so rational. Both of these are also examples of just how limited the logic of the market place really is. It’s limited because it relies on collective human behavior rather than human intellect for its logic. And this is precisely why we sometimes need government actions to supersede illogical market outcomes.

Corporate Taxes Fall as Profits Soar

The Economist states it just right. Big corporations are avoiding their tax obligation. They have no sense of duty or obligation towards the peoples government which created corporations and the condition in which they have flourished. Increasingly, government is a gadfly to corporate profit making as citizens insist, through their government, that we breath clean air, drink pure water and eat healthy foods. Corporations are so large and powerful today that the only checks on their power is big government… hence the sustained attacks they are waging on big government. But when governments no longer have the power or ability to collect taxes from the elite or the largest corporations, they are close to colapsing. That is the message I take away from this latest report. I encourage everyone to go there and read more.

Taxing for some

America’s corporation-tax receipts falter even as company profits soar

THE pressure on tax-avoiders is mounting. In the latest episode Tim Cook, Apple’s boss, was called before a Senate subcommittee to explain why the tech giant had paid no tax on $74 billion of its profits over the past four years—though it has done nothing illegal. This comes at a time when America’s corporate profits are at a record high, thanks to the swift sacking of workers at the start of the recession, lower interest expenses, and the fact that cheap labour in emerging markets has eroded union power, allowing firms to move production offshore and defy demands for pay rises. Meanwhile corporation tax, which makes up 10% of the taxman’s total haul (down from about a third in the 1950s) has plummeted. An increase in businesses structuring themselves as partnerships and “S” corporations, which subject profits to individual rather than corporate income tax, is in part to blame. But tax havens are also culprits, as they lower their tax levels to lure in bigger firms.