Home » Posts tagged 'Income'

Tag Archives: Income

Our Chronic Wage Stagnation, Symptoms and Treatments

by Brian T. Lynch, MSW

Decades of frozen wages relative to our expanding wealth is the root cause of many economic problems. More people falling into poverty, a shrinking middle class, declining retirement savings, increased welfare spending, higher unemployment, more aid to working families, declining government tax revenues, diminished funding for Social Security and Medicare, a sluggish economy (despite a record high stock market), slow job growth and heighten social tensions along the traditional fault lines of race, ethnicity and gender are among the many issues influenced by decades of wage stagnation.

Beginning in the late1970’s most American workers received only cost of living adjustments in their paychecks while their real earnings gradually diminished each year. Employers increased hourly wages to keep pace with inflation, but they suddenly stopped raising wages to reward workers for their productivity. Earned income has declined for most Americans as a percentage of our gross domestic product (GDP) This amounts to a dramatic and intentional redistribution of new wealth over the last 40 years. Nearly all this new wealth has gone to the rich and powerful.

The visual evidence of wage stagnation relative to hourly GDP is apparent in one powerful graph (below). You may have this it before.

SYMPTOMS

The effects of wage stagnation on our economy have been gradual and cumulative. Its impacts don’t raise red flags from one year to the next, but the cumulative effects are obvious. The trending rise in income inequality, for example, was missed entirely for 25 years, and then it still took another decade for it to catch the public’s attention.

According to USDA data on the real historical GDP and growth rates[i], the U.S. economy grew by $368 trillion between 1976 and 2013. That is a 109.4% rise in national wealth, more than a doubling of the national economy. Almost none of that wealth was shared with wage earners. If hourly wages continued to grow in proportion to hourly GDP, as it had for decades prior to the mid-70’s, the current median family income today would be close to $100,000 a year instead of the current $51,017 per year.[ii]

Think about that for a moment, and about all the implications for wage based taxes and payroll deductions. For simplicity sake, let’s say wages would have double if the workforce received productivity raises. That would significantly reduce the number of families currently eligible for taxpayer subsidies such as SNAP (food stamps), housing assistance, daycare and the like. At the same time the workforce would be generating much more income tax revenue.

Consider next the impact wage stagnation has had on payroll deductions. Social Security and Medicare premiums have not financially benefited from the growing economy. Double current wages and you double current revenues for these programs as well. Moreover, the economy has grown at an annual rate of 2.9% since 1976. If Social Security and Medicare had benefited from this new annual wealth, the effect on current revenue projections would be profound. We would not be looking at a projected shortfall any time in the future.

The impact of wage stagnation on consumer spending is perhaps the most insidious problem. While worker wages have stagnated, the production of goods and services has grown. How is that possible? Some of this production is sold in foreign markets, but domestic markets are still primary. And it is here where economic theories have done a disservice.

A generation of economists and business leaders have treated consumers and workers as if they were not one and the same. This has fractured how we look at the economy and given rise to the notion that labor is just another business commodity. It disguises the fact that labors wages fuel consumer spending. Wages help drive the whole economy while wage stagnation reduces consumption over time.

To overcome this effect we have seen the need for mother’s to enter the workforce in mass, and for banks to invent credit cards to bolster consumer spending. These and other creative measures can no longer forestall the decline in worker spending. So while the financial markets ride the tide of America’s growing wealth, the fortunes of those who have been cut off from that new wealth continue to slip beneath the waves.

As for social tensions among different racial, ethnic and gender groups, the effect of stagnant wages relative to the nation’s growing wealth creates a lifeboat mentality and zero sum thinking. For the first time in many generations parents are worried that their children will have less in life than they had. When the whole pie is shrinking a bigger slice by one person means a smaller piece for others. This thinking exists because for over 95% of wage earners the economic pie hasn’t grown in 40 years.

TREATMENTS

You may not be ready to accept chronic wage stagnation as “the syndrome” underlying our economic woes, but it’s also true from my experience that having solutions (or “treatment options”) at hand often makes it easier to identifying the problems they resolve. With that in mind, I want to offer some solutions to America’s low wage conundrum.

One direct approach to raising worker wages is the one currently being discussed in the public dialogue, raising the minimum wage. This benefits the lowest paid workers and also puts pressure on employers to increase pay for other lower wage earners. The current target of $10.10 per hour would still leave many families at or below the poverty line. Workers making the new minimum wage would still be eligible for some public assistance for the working poor. While passing a minimum wage law is at least possible, this option is not a systemic solution to wage stagnation. Even index the minimum wage to inflation would not compensate for declining wages relative to GDP growth.

Another direct approach to ending wage stagnation is to pass a living wage law. This would set the minimum wage at a level that would allow everyone working full-time to be financial independent from government assistance, including subsidized health care. A living wage law could be indexed to the local cost of living where a person is employed. This is idea because it takes into account local economic conditions which are determined by market forces rather than government edict. But passing a living wage law in the current political climate is unlikely.

There are other ways of encouraging wage growth that don’t involve direct wage regulation. One idea would require the federal government to recoup, through business income tax rebates, the cost of taxpayer supported aid to working families from profitable businesses that pay employees less than a living wage. Employee wages are easily identified through individual tax returns. Eligibility for taxpayer supported subsidies are relatively easy to estimate as well, so recouping public funding to support a company’s workforce is a practical possibility. A portion of the recovered money could be paid into Social Security and Medicare to make up for lost revenue due to substandard wages.

A welfare cost recovery plan could gain popular support given the growing public resentment towards taxpayer funded social programs. At least 40% of all full-time employees in America currently require some form of taxpayer assistance to financially survive. More importantly, this plan places the burden of supporting the workforce back on profitable businesses where the responsibility lies.

Another solution has been suggested by former US Labor Secretary, Robert Reich, and others. They support proposed legislation, SB 1372, that sets corporate taxes according to the ratio of CEO pay to the pay of the company’s typical worker. Corporations with low pay ratios get a tax break. Those with high ratios get a tax increase. This would effectively index worker wages to CEO compensation in a carrot and stick approach to corporate taxes. The details and merits of this approach is outlined elsewhere.[iii]

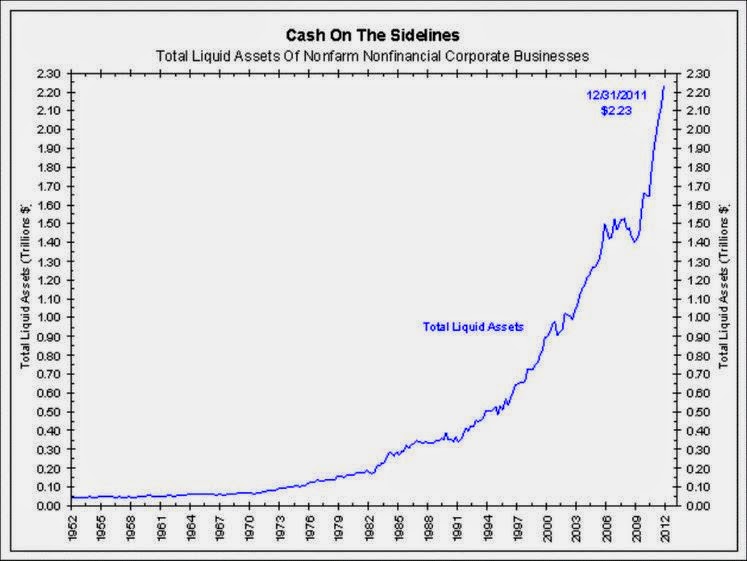

Do U.S. businesses have the financial capacity to offer higher wages to their workers? I would like to answer that question with another graph that you may also have seen before.

Credit: Blue Point Trading http://www.blue-point-trading.com/blue-point-trading-market-view-june-07-2012

There is a clock ticking somewhere in the background on this issue. There is a point somewhere in the future where it will be too late to fix wage stagnation through the normal democratic processes. History has proven this to be true. We are not at that point now, but we are past the point treating wage stagnation earnestly.

______________________________________________________

[i] Link: Real Historical Gross Domestic Product (GDP)

[ii] As of 2013 the median family income of $51,017 x GDP growth of 109.4% = $104,796 per year

[iii] Link: Raising Taxes on Corporations that Pay Their CEOs Royally and Treat Their Workers Like Serfs

Prologue To Wealth Inequality Awarness

By Brian T. Lynch, MSW

Before I had a blog, before the Wall Street “privateers of equity” crashed the economy, and long before the Occupy movement occupied anything, there were seemingly crazy folks like me trying to sound the alarm on our economy. I wrote Letters to the Editor in local newspapers and sent copies to every newspapers across the country for which I had an email addresses. What disturbed me back then was that no one in the media, or even in academia, seemed to be paying much attention. Event have consequences, and the crash in 2008 caught us flat footed.

It is unknown how social problems that exist for years suddenly become public issues to be solved. No one knows what triggers these tipping points. Even when a single individual is clearly associated with a change or a movement or a discovery (Einstein, for example), that person is responding to what ever came before. Sometime it is the consequential event rather than any alarm bells that finally get our attention. The firmament that precedes public cognition before a disastrous event remains a mystery to me.

My wife just came across one of my old letters. What startled me is that I could have written this same letter today, except the statistics are far worse now.

Here below is my Daily Record Letter to the Editor published on Christmas Eve, 2006.

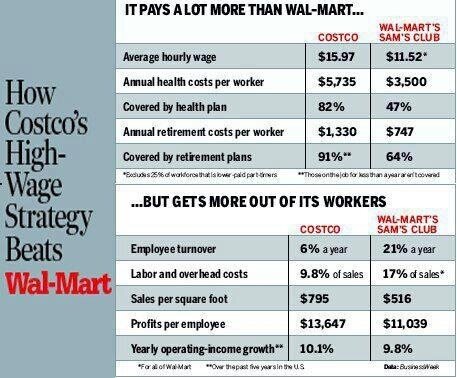

Higher Wages – Good for Families, Good for Economy & Good for Business

Below is another graphic that speaks for itself. Not only does paying higher wages improve the US economy and the lives of every citizen, it also makes good business sense.

I have written extensively on wage history and the case for a living wage, wealth distribution in America, our global business competitiveness, the dangers of our growing wealth inequality, and many other issues effecting middle and working class Americans, including and post on class warfare.

In a Labor Day message from former Secretary of Labor, Robert Reich, he, ” breaks down what it’ll take for workers to get a fair share in this economy — including big, profitable corporations like McDonald’s and Walmart to pony up and finally pay fair wages.

There is a petition that you can sign if you click on the above link. Please consider it your Labor Day obligation to those who struggled and even died to give you the benefits we still have today.

Corporations Open New Push for Even More Favorable Tax Laws

Beware America! The push is on for yet another round of self-serving corporate tax reform. A press release from the Business Roundtable announced the release of a new report touting the economic benefits of “revenue neutral” corporate and individual tax reforms. Below is a summary of the findings from the press release and a link to the report. But before you read it, consider what the real trend is in corporate tax revenues compared with what individuals contribute.

HERE IS THE TRUTH! Corporate tax rates do not reflect what corporations actually pay in income taxes, and the effective corporate tax rates, as well as the percentage of tax revenues they contribute have been in decline for decades.

Decline in Corporate Tax Burden Over 40 Years

The shift in the percentage of total taxes paid by individuals has grown substantially over the years. Individual income taxes raised 41% of the total income tax revenue in 1943 compared to 79% of total revenues today. And the shift in tax receipts from corporations to individuals cannot be explained by a shift away from C corporations (who pay the corporate income tax) to S corporations (who don’t). An analysis of that shift in corporation type is an insignificant contributor to the overall shift in the tax burden. [http://rdwolff.com/content/massive-shift-tax-burden-corporations-individuals-statistical-mirage ]

Shifting the tax burden from corporations to individuals over the past 40 years is yet another factor contributing to the current decline in domestic consumer spending. Wage suppression, the shifting of the tax burden from the rich to the middle class, coupled with the decline in the tax burden on corporations are all that is needed to explain the decline of America’s middle class, the rise in poverty and the growth of government spending in social support programs. The people are going broke, the government is going broke trying to prop us up and the rich are becoming richer and more powerful each year.

PRESS RELEASE

BUSINESS ROUNDTABLE RELEASES ECONOMIC CASE FOR CORPORATE TAX REFORM

Comprehensive Data Analysis Shows Tax Reform Would Ensure U.S. Competitiveness and Lead to U.S. Economic Growth

Corporate Tax Reform – The Time Is Now

http://usahomecourt.org/resources/business-roundtable-releases-economic-case-corporate-tax-reform

Key components of the Roundtable’s analysis include: [also known as “talking points”]

- U.S. Companies’ Fiercest Competitors Enjoy Lower Home-Country Tax Rates: It is well known that the U.S. combined (federal and state) statutory tax rate is the highest of any developed nation, averaging 39.1 percent. As the analysis points out in detail, American companies now find that their closest foreign competitors are based in countries with lower corporate tax rates and international tax systems more favorable to their global operations than the U.S. rules. Since 2000, 30 of the 34 Organisation for Economic Co-operation and Development (OECD) countries have reduced their corporate tax rate.

- High Rates are a Drag on the U.S. Economy: Researchers at Cornell and the University of London report that a one-percentage-point decrease in the average corporate tax rate would result in an increase in real U.S. GDP of between 0.4 to 0.6 percent within one year of the tax cut.

- Double Tax on Foreign Earned Income Hurts American Companies and U.S. Competitiveness: Within the OECD, of companies headquartered outside the United States, 93 percent of the world’s top 500 companies (based on Fortune’s 2012 list) are headquartered in countries that use “territorial” tax systems, where income earned abroad is not taxed again when earnings are repatriated, unlike under the current U.S. system. This is up from only 27 percent of the same countries utilizing territorial systems in 1995 – signaling a significant trend towards the more competitive method of taxation.

- Under current law, foreign earnings are effectively “locked out” of the United States: An estimated $1.7 trillion in accumulated foreign earnings was held by the foreign subsidiaries of American companies in 2011. If only half of that amount came back to the United States in response to enactment of a market-based territorial tax system, the funds freed up for use at home would exceed the increased government spending and tax relief provided under the 2009 American Recovery and Reinvestment Act.

- Effective U.S. Corporate Tax Rate 12+ Percentage Points Higher than OECD Countries: Data in the new document disproves claims of low “effective” rates (amount of tax paid after deductions) paid by U.S. corporations, citing a new World Bank study of corporate income taxes in 185 countries for 2013 that finds that tax payments are higher for companies operating in the United States as a percentage of income than the average of other OECD and non-OECD countries. In fact, the U.S. effective tax rate (ETR) of 27.6 percent is more than 12 percentage points higher than the average of other OECD countries and 11 percentage points higher than the average of non-OECD countries. The analysis also explains why using the ratio of corporate income tax to GDP is an improper measure of effective rates.

- U.S. Workers Bear the Burden of the Outdated U.S. Corporate Tax System: Corporate Tax Reform – The Time Is Now also analyzes a number of recent studies that find that workers bear between half and three-quarters of the burden of the corporate income tax. These findings suggest reducing the corporate income tax rate would provide benefits to workers through higher wages.

CLASS WARFARE – OVERVIEW OF WAGES, TAXES and WEALTH IN AMERICA

Since Reagan in 1980’s Tax Rates for the wealth were cut in half and capital gains tax (where most make their money) was cut in half again. http://j.mp/ZFFQHB

Wages and GDP rose together until wages were suppressed in the 70’s, otherwise median income today would be greater than $100K instead of $51K http://j.mp/14MoT67

The combination of wage suppression and the collapse of the upper income tax brackets is the cause of our wealth and income inequality today. http://j.mp/102YbAk and http://j.mp/10DVrLn

A majority of American’s don’t make enough money to support a robust economy because a handful of us have more money than they can spend. http://j.mp/16E3zOT

Current US policy is creating permanent income inequality. Income mobility is shrinking as income caste system forms. http://t.co/nK5uFGyCaG

We know what victory looks like in Class Warfare. It’s the formation of an income caste system where birth determines your level of success. http://j.mp/Y1HwQP

Obama’s proposed raise in min. wage from $7.20 to $9/hr would mean a person working 40hr/week at min. wage would still be below poverty line. http://j.mp/10DwY7V

If the minimum wage was raised to $18/hour the Federal Government could eliminate almost all aid to the working poor, saving tons of money. http://j.mp/10DVrLn

Every tax dollar paid to assist the working poor is a tax subsidy providing their employer a federally funded labor discount. http://j.mp/16Bml7r

God! When are we going to wake up?

Permanent Inequality Rising Over Past Two Decades

A Spring 2013 BPEA paper by Vasia Panousi, Ivan Vidangos, Shanti Ramnath, Jason DeBacker and Bradley Heim

Disadvantaged Becoming Worse Off Long-term; Tax System Has Helped But Not Significantly

Income inequality in the US has increased in recent decades, and this increase is of a permanent nature, according to a new paper presented today at the Spring 2013 Conference on the Brookings Papers on Economic Activity (BPEA).

In “Rising Inequality: Transitory or Permanent: New Evidence from a Panel of U.S. Tax Returns” … [the authors] use new data to closely examine inequality, finding an increase in “permanent inequality” — the advantaged becoming permanently better-off, while the disadvantaged becoming permanently worse-off. The paper has important public policy implications because rising income inequality will lead to greater disparity in families’ well-being that is unlikely to reverse, whereas “transitory inequality” or year-to-year income variability would imply greater income mobility—those who fare worse today might be able to do better in later years. The authors are among the first to examine various measures of income in great detail, including earnings from work activities as well as broader measures of family resources such as total household income. [SNIP]

Looking at the impact of tax policy on inequality, the paper finds that although the U.S. federal tax system is indeed progressive in that it has provided some help in mitigating the increase in income inequality over the sample period, it has, however, not significantly altered the broadly increasing inequality trend. All told, the results suggest that rising income inequality will likely lead to greater disparity in families’ well-being and reduce social welfare in the long-run.

Rising Inequality: Transitory or Permanent?

New Evidence from a Panel of U.S. Tax Returns

Click to access 2013a_panousi.pdf

Abstract

We use a new, large, and confidential panel of tax returns to study the permanent versus-transitory nature of rising inequality in individual male labor earnings and in total household income, both before and after taxes, in the United States over the period 1987-2009. We conduct our analysis using a wide array of statistical decomposition methods that allow for various flexible ways of characterizing permanent and transitory income components. For male labor earnings, we find that the entire increase in the cross-sectional inequality over our sample period was permanent, that is, it reflected increases in the dispersion of the permanent component of earnings. For total household income, the large increase in inequality over our sample period was predominantly, though not entirely, permanent. For this broader income category, both the permanent and the transitory parts of the cross-sectional variance increased, but the permanent variance contributed the bulk of the increase in the total. Furthermore, the increase in the transitory component reflected an increase in the transitory variance of spousal labor earnings and investment income. We also show that the tax system partially mitigated the increase in income inequality, but not sufficiently to alter its broadly increasing trend over the 1987-2009 period.

Capital Investment Income Drives Income Inequality

A recently published analysis by Thomas L. Hungerford (see highlights below) looks at factors driving the growth of income inequality for the period between 1991 to 2006. Hungerford looked at the contributing impact of three factors, tax policy, labor wages and capital income. During the studied period he found that capital income (capital gains, interest income, business income and dividends) was by far the largest factor contributing to rising income inequality. Wages and salaries alone were not a factor and tax policies were only a minor contributor during this period, largely due to the more favorable tax treatment of capital gains.

This report doesn’t trace the history of income inequality prior to 1991 where changes in wage growth in the late 1970’s and the collapsing of upper income tax brackets in 1980 and 1985 were more dramatic.

It is worth remembering that for most of the past 100 years capital gains was treated as ordinary income for tax purposes. In recent times, capital gains have be treated as a separate class of income with a more favorable tax treatment. Capital ownership has always been more concentrated at the upper end of the income/wealth continuum. Capital is, of course, an ownership stake in our economy whether through stocks, bonds, property or business ownership. The income generated when these capital investments are bought and sold is currently taxed at 15% (if it is held for more than a year). That is less than half the top tax rate for wages and salaries. And how is capital ownership distributed in America?

Who Owns What In America?

The distribution of wealth ownership, as opposed to income inequality, is even more skewed towards the wealthy as the pie chart below shows. The whole pie represents the total wealth in America. Each of the five slices of the pie represent 20% of the US population according to how much wealth they own.

The slice of ownership for the poor and working poor are barely visible. Eighty-percent of all Americans own just 15.6% of America’s wealth. The number of people who slipped into poverty in 2010 was at an all time high of 46.2 million, so the poorest 20% of all Americans, in terms of wealth ownership, includes 15.5 million who are technically above the income poverty line. The poorest 40% of Americans essentially own almost nothing while the top 20% own almost 85% of everything. As a result, favorable tax policies for capital gains income has a highly disproportional benefit for the wealthiest Americans. Capital income for this wealthy segment is what drives rising income inequality today.

______________________________________________________________________

Changes in Income Inequality Among U.S. Tax Filers Between 1991 and 2006: The Role of Wages, Capital Income, and Taxes

Thomas L. Hungerford

thunger@starpower.net

January 23, 2013

Electronic copy available at: http://ssrn.com/abstract=2207372

HIGHLIGHTS FROM THIS REPORT:

Research has demonstrated that large income and class disparities adversely affect health and economic well-being (see, for example, Marmot 2004, Wilkinson 1996, Frank 2007, Singh and Siahpush 2006).

Research has shown, however, that income mobility [in the United States] is not very great and the degree of income mobility has either remained unchanged or decreased since the 1970’s (Hungerford 2011, and Bradbury 2011).

Earnings inequality has been increasing since at least the late-1960s (Kopczuk, Saez, and Song 2010). [The] CBO (2011) has documented that income inequality has been increasing in the United States over the past 35 years.

Three potential causes of the increase in after-tax income inequality between 1991 and 2006 are examined in the analysis: changes in labor income (wages and salaries), changes in capital income (interest income, capital gains, dividends, and business income), and changes in taxes.

Increased salaries paid to CEOs, managers, financial professionals, and athletes, is estimated to account for 70 percent of the increase in the share of income going to the richest Americans (Bakija, Cole, and Heim 2010).

A declining real minimum wage could affect lower income tax filers (the inflation-adjusted minimum wage fell from $6.57 per hour in 1996 to $5.57 per hour in 2006).

Income of the richest 0.1 percent of taxpayers is sensitive to changes in asset prices and this may have been especially important in the increase in the income share of those at the top of the income distribution (Bakija, Cole, and Heim 2010).

Frabdorf, Grabker, and Schwarze (2011) also find that capital income’s share in disposable income has increased in recent years in the U.S. and show that capital income made a large contribution to income inequality in relation to its share in income.

While the individual income tax system is progressive and has been since it was introduced in 1913, the trend has been toward lower marginal tax rates and a less progressive tax system (Piketty and Saez 2007, and Alm, Lee, and Wallace 2005). As a result, the tax system may be less able to equalize after-tax incomes.

The major tax changes between 1991 and 2006 were (1) the enactment of the Omnibus Budget and Reconciliation Act of 1993 (OBRA93), which increased the top marginal tax rate from 31 percent to 39.6 percent, and (2) the enactment of the 2001 and 2003 Bush tax cuts, which reduced taxes especially for higher-income tax filers. The Bush tax cuts involved reduced tax rates, the introduction of the 10 percent tax bracket (which reduced taxes for all taxpayers), [it also] reduced the tax rates on long-term capital gains and qualified dividends. In 1991, long-term capital gains were taxed at 28 percent (15 percent for lower-income taxpayers) and all dividends were taxed as ordinary income. The next year, the

long-term capital gains tax rate was reduced to 20 percent. By 2006, long-term capital gains and qualified dividends were taxed at 15 percent (5 percent for lower-income taxpayers). Tax policy changes that affect progressivity will affect after-tax income inequality (Kim and Lambert 2009, and Hungerford 2010).

Hungerford (2010) notes, however, that about 75 percent of families contain just one tax unit (another 17 percent contain two tax units with the second tax unit usually a cohabitating adult or a working child that cannot be claimed asa dependent on another tax return). Consequently, most of the tax units likely represent a family.

Piketty and Saez (2003) argue that capital gains are not an annual flow of income and have large aggregate variations from one year to another; they exclude capital gains from much of their analysis. Blinder (1980) argues that capital gains should not be included in income because what is important is real accrued capital gains [cashed out]. Also, that capital gains represents partial maintenance of in an inflationary world. [in other words, gains shouldn’t be taxed as it serves as an inflation adjustment for capital]

capitals gains have increasingly become an important source of compensation for corporate executives (through stock options), and private equity and hedge fund managers (carried interests). Consequently, income from capital gains is included in the analysis.

Several recent studies estimate that most or all (in some cases more than 100 percent) of the burden of the corporate income tax falls on labor through reduced wages [while] other evidence suggests that most or all of the burden of the corporate income tax falls on owners of capital. [So take your pick!]

Federal individual and corporate income taxes had an equalizing effect on inequality regardless of the inequality measure. Federal taxes had a slightly greater equalizing effect in 2006 than in 1991—taxes appear to have been slightly more progressive in 2006 than in 1991. The top marginal tax rate in 1991 was 31 percent compared to 35 percent in 2006; the lowest tax marginal rate was 15 percent in 1991 and 10 percent in 2006. However, the increased equalizing effect of the individual income tax is likely due to bracket creep—more income is taxed at the highest rates—than to tax law changes. Tax policy changes appear to have played a direct role: OBRA93 tended to have an equalizing effect on after-tax income while the 2001 and 2003 Bush tax cuts tended to have a disequalizing effect.

Tax policy may have also have had an indirect effect on rising income inequality, especially between 2001 and 2006. The reduction in the tax rate on long-term capital gains and qualified dividends may have led to the increased importance of this source in after-tax income.

Overall, changes in [wage] labor income does not appear to be a significant source of increased income inequality between 1991 and 2006. Wages had no or a small disequalizing effect when other inequality measures are used.

By far, the largest contributor to increasing income inequality (regardless of income inequality measure) was changes in income from capital gains and dividends. Capital gains and dividends were less equally distributed in 1991 than in 2006, though highly unequally distributed in both years.

__________________________________________________________

Thomas L. Hungerford currently works at the Congressional Research Service (CRS) which is part of the Library of Congress. The CRS provides the policy and legal analysis to Congressional committees and Members, regardless of their party affiliation. CRS staffers sometimes do reports on their own. Hungerford says this report, “… [does] not reflect the views of the Congressional Research Service or the Library of Congress.” Hungerford is well-published in the professional literature. He has worked for the Social Security Administration, the Office of Management and Budget, and the General Accounting Office in the past. The excerpts highlighted here are of my own. You are encouraged to read the full study at the URL address provide above.

Raising Wages Would Revive Our Economy

It seems so obvious that consumption is the fire that powers an economy and money is the fuel. It doesn’t matter from where the spending comes in the short run, but it must come from ordinary people in the long run. Wages paid are dollars spent and a dollar spent is a dollar earned in a free economy. Just as you can dampen consumption by raising the cost of borrowing, you can also dampen consumption by suppressing wages, which is exactly what we have been doing for more than 30 years. Corporations have become cash rich but customer poor. They could end this sluggish economy tomorrow by raising wages.

A 99 Year History of U.S. Income Tax Rates

SPECIAL NOTE: Our US progressive tax structure [or whats left of it] will turn 100 years old on October 3rd. We should plan a celebration!

OUR TAX STRUCTURE USE TO BE MUCH MORE PROGRESSIVE THAN IT IS TODAY.

The Progressive Tax Code

Our progressive, or graduated income tax was signed into law by President Woodrow Wilson On October 3, 1913. The idea was to create a system where those who did well bore a greater responsibility for funding the government. In fact, the original intent was to only tax the wealthiest citizens. The income tax was never meant to burden the majority of wage earners. The new law taxed individuals making $3,000 or couples making $4,000 per year. $4,000 at that time would be equivalent to about $100,000 per year in today’s dollars. What the law did not take into account was inflation. Much the same as is presently the case with the minimum alternative income tax, the original income tax brackets stayed constant every year while inflation and working class wages slowly rose. Eventually, income taxes became a burden to lower wage earners as well as the rich. [ http://www.buzzle.com/articles/the-controversial-history-of-the-graduate-income-tax.html ]

The progressive nature of the income tax is achieved by creating multiple income tax brackets to for rising levels of income. Each tax bracket has a slightly higher tax rate. Between 1913 and 1918 the number of tax brackets that applied to wealthy incomes rose to 56 brackets. By 1940 that number of brackets fell to 24 and there it more or less remained for the next 40 years.

What did rise over this time period were the marginal tax rates. By the 1950’s the top marginal tax rate for the wealthiest earners was 90 percent. The top marginal tax rate was gradually lowered over the next 30 years until it was at 70% in 1980. In 1981 President Ronald Reagan collapsed the top 9 tax brackets to lowered the top marginal tax rate from 70% to 50%. During is second term he eliminated 10 more upper tax brackets dropping the top marginal tax rate from 50% to just 28%. He also raised the tax rates on the lowest income earners, those who were originally not expected to contribute. At the same time, tax breaks for the wealthiest Americans combined with huge jumps in military spending resulted in huge budget deficits and a large national debt that has been with us since.

The top marginal tax rate for wage income was eventually raised back to 35% but not before capital gains income was stripped from the progressive tax code and separately taxed at a rate of just 15%. Capital gains income represents the major source of income for the wealthiest Americans. So the original intent of the progressive tax code, that the tax burden should only fall on the wealthiest American’s, was turned upside down.

For a glimpse of the problem with our current tax structure, see the US states map at the following URL to see how much more the bottom 20% are paying in taxes, as a percentage of income, over the top 1%. http://tiles.mapbox.com/occupy/map/TaxBurden

The graph below shows the 99 year history of tax rates for four incomes levels in the US. The data are adjusted for inflation and reflect the current value of the dollar. Tax rates for those making one-million dollars are in blue, those making $100,000 are in pink, those making $50,000 (approx. median household income) are in brown, and those making $25,000 (half of all American make less than $26,364) are in black. All rates are based on the married, filing jointly category. The tax information begins in 1913 and continue through 2011.

See data source here: http://taxfoundation.org/article/us-federal-individual-income-tax-rates-history-1913-2011-nominal-and-inflation-adjusted-brackets

What the graphic says to me is that for most of the last 100 years the wealthiest Americans have been paying more taxes than they are today, a lot more. Also, there was a period from around 1932 to 1988 when tax rates were lower for the working poor than for middle Americans.

I also noticed that beginning in the early 1980’s the tax brackets for the wealthy began collapsing until 1987 when a person making a million dollars a year was paying the same tax rate as someone making $117,760 per year. This had the effect of adding millions of tax payers into the same federal tax bracket as the ultra-wealth. From a political perspective, they became a single voting block on the issue of taxation. Also note that the tax rates for the two lower incomes jumped significantly in 1942-1946 and has been relatively steady since, decreasing only slightly during the Reagan administration when taxes on the wealthiest Americans began dropping sharply. Remember that mantra in the 80’s, “It’s not what you make, it’s what you keep.” This was never truer than for the wealthiest among us.

See Raw Data Here

http://www.taxfoundation.org/files/fed_individual_rate_history_nominal&adjusted-20110909.pdf

The Rise and Fall of the US Progressive Tax Structure

Below is a companion chart to the 99 Year History of Tax Rates in America (Click Here to see chart). This graph charts the number of tax brackets into which income was divided over the years. Looking back, it is apparent that our progressive tax structure had many more tax brackets separating rich and poor for most or hour history. There was a peek of 56 income tax brackets in 1918. In 1924 (the Roaring 20’s) that number was compressed to just 23 tax brackets. The number of tax brackets fluctuated over the next 62 years but maintained an average of 25 brackets until the 1980’s.

In 1981 the first of Ronald Reagan’s tax cuts was passed dropping the top tax rate from 70% to 50%. Five years later his Tax Reform Act of 1986 dropped the top tax rate again to 28% while raising the bottom rate from 11% to 15% where it remains today. The 1986 law also collapsed the number of tax brackets from 15 in 1984 to 5 in 1985. While lowering the top tax rate for the rich from 70% to 28% was a huge boost for the wealthiest Americans, compressing the top 10 tax bracket helped assure that the changes would not be undone. The reduction in tax brackets meant that the number of people in the top earners bracket went from tens of thousands of the riches voters to many millions of voters including those with much more modest incomes. By lumping together people making over $300,000 with those earning many times that amount the change created a large voting block of voters who would oppose future tax hikes.

During these same years the Reagan administration began deregulating the banking and finance industries leading to more and more wealth building opportunities for those already blessed with riches. Ronald Reagan was following the economic path created by the economist, Milton Friedman, who, in turn, was influenced by the Objectivism philosophy of Ayn Rand. Ayn Rand believed that altruism and self-sacrifice for others is evil. See more here]

Graphic View of Wealth Distribution in America

Who Owns What In America?

Imagine lining up everyone in America according to what they own, starting with those who own nothing and continuing down the line to those who own a lot. Now divide that line of people into five equally long segments. Each segment would include 20% of the total population, or about 61.7 million people. Next, add up the total amount of what everyone owns in each segment. The result is represented by the pie chart below. The whole pie represents the total wealth in America. The size of each slice represent the ratio of how much each segment owns of America’s wealth. The slice of ownership for the poor and working poor are barely visible. 80% of all Americans own just 15.6% of America’s wealth.

The number of people who slipped into poverty in 2010 is an all time high of 46.2 million, so the poorest 20% in terms of wealth ownership includes 15.5 million folks who technically don’t meet the poverty criteria, based on income levels. The poor essentially own almost nothing. The working poor own twice of almost nothing.

When I first plotted the distribution of wealth in America in this pie chart it reminded me a little of that Pac-Man character. The richest Americans own 84.6% of everything while the remaining 80% of us have 15.4% left. The statistical middle of what I labeled the “Middle America” owns just 4% of America’s wealth assets.

This raises an interest question. How do we define middle class? Is Middle America, as I’ve labeled it here the same as middle-class?

No, We usually define middle class by income levels, not wealth ownership. As of 2011 the median family income has declined to just over $51,000 per year. If we were to define middle class based on 10% of families above and below the median income (as I have done here for wealth ownership, the narrow and very low income range would not fit most peoples conception of “middle class”.

But this pie chart displays the distribution of wealth, not income. It includes all equity ownership in everything from homes to 401K’s, stocks, bonds, businesses, etc. This chart cannot be directly converted to income levels. There are people with equity but not much income and people with large incomes but not much equity.

However, from a visual perspective the median income (middle most income) will still fall somewhere near the center of the red colored slice, about where the label line is drawn. Individuals in that group made about $26,364 per year, or about $52,000 per household in 2010. Beyond that it is difficult to superimpose income brackets on this pie chart

This graphic really make clear just how compressed wealth distribution is in America. Missing from the public dialogue over the past few decades is mention of the working poor. Politicians and the media seem to focus on the middle class or the poor as if there were no working poor.

The other conclusion I come away with is that there is plenty of wealth here in the still wealthiest nation on Earth. Telling ourselves that we can’t afford social services for the poor or good public schools or what ever else we desire as a nation is simply not true. As a nation we can afford a much better society than we have now.