Home » Posts tagged 'Taxes'

Tag Archives: Taxes

New Jersey’s Regressive Public School Funding

by Brian T. Lynch, MSW

New Jersey recently published the annual “Taxpayers Guide to Educational Spending”. The headline in the Star Ledger was that school spending is up 5% over last year. This is hardly news given that inflation alone accounted for 1.7% of the increase.

Much of the remaining 3.3% increase in school spending is structural by design. Consider that new teacher salaries start low and increase annually as they gain experience. We also compensate teachers as they obtain higher educational degrees as a means of improving the quality of our teachers. Add to this the fact that the total number of teachers gradually increase as student enrolled numbers creep up a little every year. Then there is the higher than inflation increases in fuel costs that drive up the cost of student transportation each year. The retirement of higher paid teachers and administrators don’t quite balance out these other factors.

What irks the public most about this 5% increase is really the story behind how we fund public education in New Jersey. It just seems unfair. And when you look under the hood, it really is unfair. Wealth based public school funding is regressive in nature. It favors the wealthy and disfavors the poor. What it costs to educate a child doesn’t vary that much between wealthy and poor school districts, but the value of property and therefore the tax base varies a lot. In today’s economy especially, the prosperity in wealthy school districts is growing rapidly relative to per pupil costs while property values in less prosperous school districts are in decline.

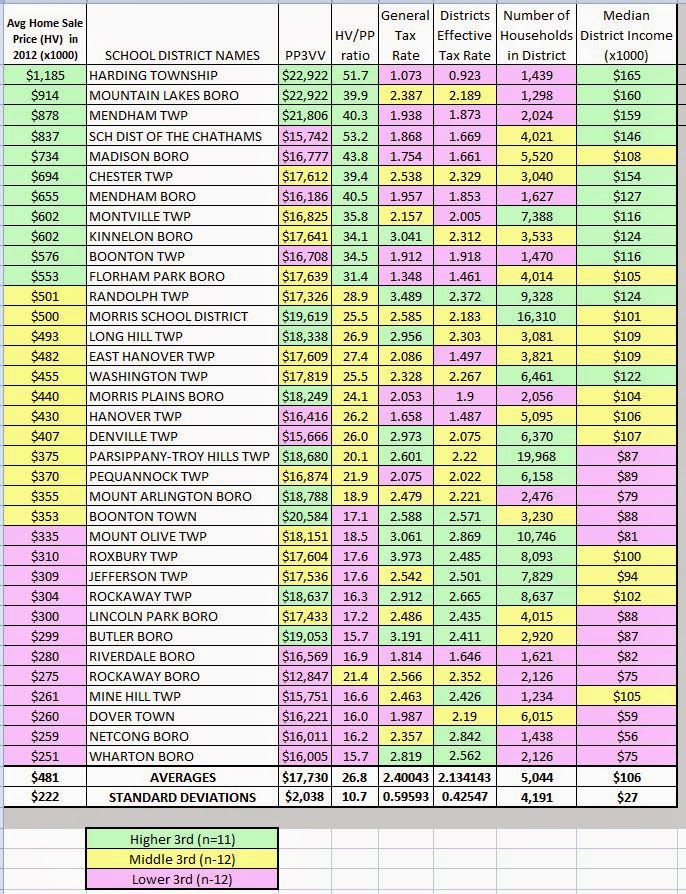

To understand the disparity of wealth based public education funding, let’s take affluent Morris County as an example (located in the central most area of the Northern half of the State). Morris County has many wealthy school districts, such as Harding where the average home sells for over a million dollars. It also has districts like Wharton where the average home sells for a quarter of that amount, or about $251,000. Property values in Dover are a bit higher, but the median family income in the Dover school district is just $59,000 compared with $160,000 per year in Mountain Lakes. (Fig.1 below)

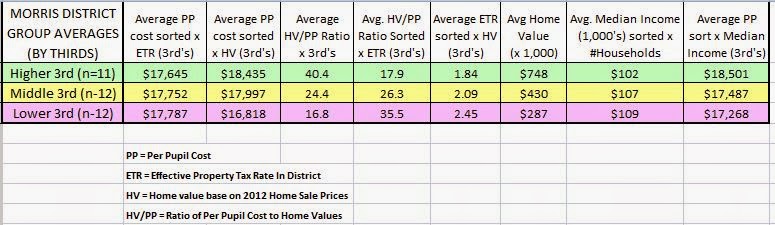

One way to gain some perspective on property based school funding is to compare what it costs to educate a student with what it costs to buy a home in the same district. In the eleven wealthiest districts of Morris County, home prices are 30 to 50 times more than the educational cost per pupil. Home values are just 16 to 18 times more than per pupil costs in the 12 poorest districts. As a general rule, the higher a district’s property values, the lower the tax rates. The reverse is usually true in poorer districts. Districts with lower property values, and lower income levels, generally have higher tax rates. While the 11 wealthiest districts in Morris County pay a little more to educate children in their district, their property tax rates are about one-third less than in the 12 poorest districts. (Fig. 2 below)

The dramatic contrast between home values and per pupil costs is partially masked when just comparing tax rates because, in the suburbs, wealthier districts tend to have fewer households. Fewer household to share the tax burden mean higher tax rates to generate sufficient revenue. Despite this fact, tax rates in 8 or the 11 richest districts is among the lowest in Morris County. Only three of these wealthy districts have higher per pupil costs while three have among the lowest per pupil costs. This highlights the fact that education costs are similar across the county. The average district cost per pupil is $17,730, plus or minus $2,038. There are a few outliers in either direction.

Educational costs vary far less than home values from district to district, so families in wealthier districts have a far easier time affording public education than families at the lower end of the economic ladder. While New Jersey’s State School Aid formula is supposed to help balance school funding across all districts, it does little to correct the underlying inequality and unfairness of wealth based educational funding.

Sources

Taxpayers’ Guide to Educational Spending 2013: http://www.state.nj.us/education/guide/2013/

General Tax Rates : http://www.state.nj.us/treasury/taxation/pdf/lpt/gtr13mor.pdf

Average Home Sales : NJ Spotlight News @ http://www.njspotlight.com/stories/13/02/28/average-home-sales-prices/ For March 1, 2013

Median Income and # Households: http://www.njspotlight.com/stories/13/12/19/median-income/

Figure 1

Figure 2

Coal Ash Disaster Turns Capitalists into Socialists (Again)

by Brian T. Lynch, MSW

Commentary:

Coal ash is what’s left after coal is burned. It’s a toxic stew containing heavy metals including arsenic, lead and mercury. For many years Duke Energy has mixed coal ash with water and pumped this cocktail from coal fired power plants into huge open pits. In February, one of the sludge pits located in North Carolina began releasing millions of gallons of toxic coal ash into the Dan River, a source of public drinking water for thousands of people.

Photo and article: http://www.salon.com/2014/02/26/north_carolina_might_finally_crack_down_on_duke_energy_after_disastrous_coal_ash_spill/

Duke Energy spent millions over the years to keep government from properly regulating their waste products. For all those decades the stockholders and upper management of Duke energy have profited from this arrangement. Now that the inevitable has occurred, clean up effort will take years and cost a billion dollars. Millions more will have to be spent to correct the improper disposal problems that Duke Energy has practiced for decades.

Safely storing coal ash should have been a cost of doing business for Duke Energy all along, but they have deferred that cost to boost their profits. Now Duke Energy’s president and CEO, Lynn Good, thinks taxpayers should bear the cleanup costs. She said, “Ash pond closure has been a plan for very long time. And because that ash was created over decades for the generation of electricity, we do believe that ash pond disposal costs are ultimately a part of our cost structure.” She believes the burden of this clean up should be shared by everyone equally. (Corporate socialism? Again?)

Corporation are legally obligated to maximize profits for their shareholders. This would be fine if they were also legally obligated to paid the full cost of doing business without cutting corners. Cleaning up toxic spills is far more expensive than preventing themand regulations to enforce safe disposal are less expensive in the long run. But asking the victims of their environmental crimes to pay for cleaning up their mess and fixing their problem should not be an option.

(See also: http://www.politicususa.com/2014/03/14/republican-hypocrites-force-nc-taxpayers-pay-duke-energys-toxic-coal-ash-dumping.html )

Bogus Claim: Obama Uses IRS to Buy Votes

There appears that a phony new scandal is taking shape on some conservative corners of the internet. It may or may not gain traction, but it is worth a peek. David DeVine, on the Website entitled TheWestern Free Press, and others, are accusing President Obama of using the IRS to create “de facto amnesty” for illegal aliens. It has to do with an aspect of federal tax law that has been ignored for years.

Here is the actual claim:

ITIN amnesty scam empowers Obama IRS to buy votes

“Outraged that illegal aliens claimed child-tax-credits, but no outrage that current tax law allows them to report income and pay taxes without threat of deportation?”

Apparently some on the right have finally discovered that many resident aliens actually do have IRS identification numbers that allow them to file and pay their federal income taxes and receive some tax benefits.

For years now rightwing conservatives have complained that undocumented aliens (by which they usually mean all non-citizens of color) don’t pay taxes and are a burden to taxpayers. This has never been entirely true, of course. Even setting income taxes and payroll deductions aside, all resident aliens pay sales taxes, property taxes (sometime indirectly by paying rent), gas taxes, cigarette taxes, tolls, fees , etc. But the biggest misconception has been that most resident aliens don’t pay income taxes. Many, perhaps most resident aliens do pay income taxes. Even my liberal friends have had a hard time believing this.

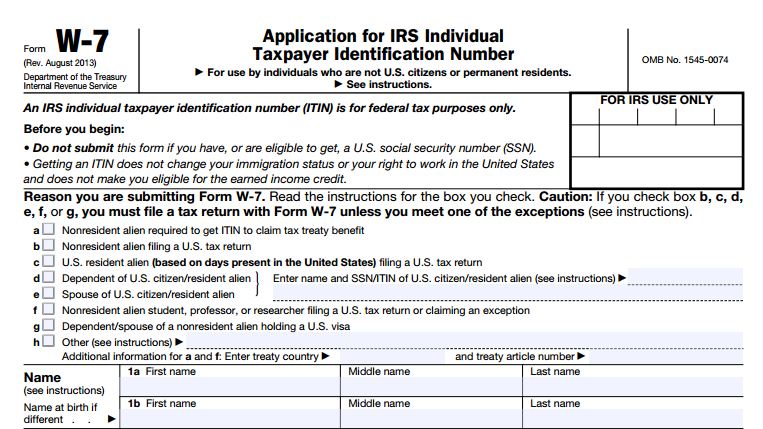

For more than forty-years the IRS has issued a nine-digit Individual Taxpayer Identification Number ( IRS application form W-7) to resident aliens who are not eligible to apply for Social Security. These identification numbers may be issued to resident aliens who earn income in the U.S. and either have a “Green Card” eligibility or meet the “Substantial Presentence” eligibility test. In fact, the instructions on the W-7 states, “A foreign individual living in the United States who does not have permission to work from the USCIS, and is thus ineligible for a SSN, may still be required to file a U.S. tax return”, and therefore obtain an Individual Taxpayer Identification Number (ITIN). So regardless of how a foreign citizen came to be here, if they earn money while here they are required to file income taxes. For example, a foreign citizen who came here in January and earned money and is still here in December must file income taxes and apply for the ITIN by attaching the application to their return.

Depending on their status and circumstance they may also be eligible to receive federal tax rebates and some other benefits under the tax law for themselves or their dependents. This includes the Child Tax Credit when a dependent child is a citizen or meets criteria in the IRS code. What resident aliens cannot collect is the Earned Income Tax Credit. It says so right on the ITIM application.

These IRS issued ITIN’s have be around at least since the 1960’s but some on the right what to use this rediscovered revelation to accuse President Obama of buying votes by making the IRS issues Child Tax Credits to “illegals.” This claim ignores the fact that all resident aliens are ineligible to vote. Some conservatives also want to pin on Obama their outrage that undocumented aliens are even allowed to report income without the threat of deportation. They would prefer, I suppose, that undocumented aliens be exempt from paying income tax, or else forced to hide their income out of fear of instant deportation.

Immigration enforcement is not the job of the IRS. It is their job to collect taxes on all residents who earn income regardless of whether they are citizens. It will be interesting to see if this issue gains traction or finds its way into round 2 of the immigration reform debate on the horizion.

The Real IRS Tax Scandal

by Brian T. Lynch, MSW

Here is the Internal Revenue Service controversy in a nut shell. Rank and file IRS agents used search terms such as “tea party” to triage a mountain of applications for tax exempt status. What the agents were trying to identify were applications where the purposes of the organizations were primarily political. Under IRS regulations, organizations applying for 501(c)(4) tax exempt status must primarily be involved in social welfare activity. All the triaged applications were eventually approved. Virtually everyone agrees the IRS must be politically neutral, so the methods the agents used to organize their workload is not an acceptable practice.

This principle and these core facts are not in dispute by anyone familiar with the details. The partisan contentions understandably arise from the lengthy inaction by senior IRS officials to end this practice. Were senior managers incredibly blind to what agents were doing or did they turn a blind eye? If it was the latter, did they ignore the practice for practical reasons or political reasons? Who up the political chain of command knew of the practice and when did they learn about it?

As happens often in today’s politically charged atmosphere, the partisan conflagration set off by the revelations is sucking all the oxygen out of the room leaving no one to explore why these practices developed in the first place. The “scandal” is a media induced distraction from much more serious problems under the surface. Among the questions we should be asking are these:

Is there an increase in tax exempt applications and is the increase asymmetrical?

Probably so, although the assessment of this is indirect. According to an analysis of data released by the IRS in response to the criticism, Martin A. Sullivan of TaxAnalysitst.org found that among the tax exempt applications approved by the IRS about two-thirds were submitted by conservative organizations. The remainder were either liberal leaning organizations or politically neutral. According to Professor Rob Reich in the April/May Boston Review, there has also been an unprecedented growth in the number of charitable foundation, or 501(c)(3) organizations. He attributes this to the growing wealth of the richest Americans. They are establishing foundations to leave a legacy and project their political influence on society from beyond the grave. So far, according to the IRS and other sources, there does appear to be a sharp increase in 501(c)(3) and (4) applications for tax exempt status. It also appears that this increase in applications are skewed towards conservative organizations and wealthy donors.

Is there a problem with tax exempt 501(c)(3) and (4) organizations being too overtly political, and if so, is the problem asymmetrical?

Image of Karl Rove by chicagopublicmedia/Flickr

According to some sources, since the Supreme Court’s Citizens United case there has been a growing number of wealthy people and corporations creating charitable foundations and social welfare organizations through which predominantly political messages are being delivered to the public, tax free. Just as we have increasingly been subsidizing big business through corporate welfare, we may now be subsidizing political messaging campaigns directed at us.

Here is an experiment readers can replicate for themselves. Type “left wing organizations” in a Google search. You will see that two right wing organizations and one left wing organization pop up. The first of these is discoverthenetwors.org, a “Guide to the Political Left” put out by David Horowitz’ Freedom Center Foundation. This guide is an alphabetical listing of allegedly left wing organizations, but looking down the list you will see it lumps together such “subversive” left wing organizations as the AARP and Abu Nidal. Abu Nidal is a Middle-East, “Spinoff of the Palestine Liberation Organization… [that] Has killed or maimed more than 900 people in over 20 countries.”

According to it’s mission, “The David Horowitz Freedom Center combats the efforts of the radical left and its Islamist allies to destroy American values and disarm this country as it attempts to defend itself in a time of terror.”

Painting the American left as affiliates of Islamist terrorists (or other notorious dictatorships as seen in on other sites) is a common theme on some conservative websites. This information is what passes as a public educational service justifying tax exempt status. Additionally, the site contains ads, which may or may not be paid advertizing. The site does claim to be 501(c)(3) tax exempt and solicits the viewers tax exempt donations.

The next organization on the search list is the Western Center for Journalism. It bills itself as a 501(c)3 tax exempt foundation and accepts tax exempt donations, yet it describes itself as a conservative organization and promotes a book written by the organizations current president, Floyd Brown. Brown’s latest book, “Obama Enemies List: How Barack Obama Intimidated America and Stole the Election”, was released in January 2013. Virtually all of the contents on this site are partisan in topic and perspective. One article by Steve Baldwin, for instance, starts out this way:

” Very few Americans realize there exists a large network of far left philanthropists and foundations in America dedicated to destroying the American way of life, our Christian-based culture and our free enterprise system. They seek to remove America from its constitutional foundations and move it toward a European-style socialism. Much of this effort is coordinated by a little known group called the Tides Foundation and its related group, the Tides Center.”

So I looked into the Tides Center and found it to be a 501(c)(3) organization dedicated to fund projects related to:

“ Art & Film, Civic Engagement, Civil Discourse, Community Development, Disability Rights, Economic Justice,’ Economic Opportunity, Education/Training, Environmental Sustainability, Faith & Spirituality, Food & Agriculture, Health Services/Healthcare Reform, HIV/AIDS, Housing/Homelessness, Human Rights, Immigration, International Development, LGBT Issues, Media ,Native Communities, Nonprofit Spaces, Peace & Conflict Resolution, Professional Development, Racial Justice, Reproductive Justice & Health, Technology, Women & Gender, Youth Development & Organizing”

Donations to the Tides Center are tax exempt, but other than its support for some issues unpopular with conservatives you will find nothing overtly political on the web site.

The third organization on the Google search list is the RightWingWatch.org operated by People for the American Way. This is a liberal organization. RightWingWatch was on the search list in connection with an article refuting a claim by Rick Joyner that Timothy McVeigh (Oklahoma City Bomber) was actually a left wing radical, not a right wing terrorist. Rick Joyner is the founder and executive director of MorningStar Ministries and Heritage International Ministries. He is also the Senior Pastor at the MorningStar Fellowship Church, a tax exempt organization.

People for the American Way bills itself as a 501(c)(4) organization, but they don’t use our tax money. When you donate you get this disclaimer:

“Because we lobby Congress, donations to People For the American Way, a nonprofit 501(c)(4) organization, are not tax deductible.”

In contrast, Freedom Works Foundation is a conservative non-profit organization. It is currently headed by former U.S. House Majority Leader Dick Armey, a Republican. The site say it is inspired by the leadership of Barry Goldwater and Ronald Reagan. It’s content is distinctly and exclusively conservative. If you press the icon to donate to the foundation web site you are taken to the donation page for Freedom Works (without the word “foundation”) which is a political action organization. There you will be given a choice to donate, “… where my donation will be used directly in the fight in Washington,” or “… where my donation will be 100% tax deductable and will be used for education, research and other efforts.” So the Freedom Works Foundation, which is tax exempt, shares the donation page of Freedom Works, which isn’t tax exempt.

Now, for symmetry sake, Google “right wing organizations.” The first three organizations (excluding the C.S. Monitor) on the search list are People for the American Way (or RightWingWatch), which does not count donations as tax deductions, the PublicEye.org operated by a tax exempt group named Political Research Associates, and Common Dreams, also tax exempt. The Common Dreams link is to a three paragraph article on the resignation of the IRS commissioner. It isn’t particularly political. The People for the American Way provides an extensive list of right leaning organizations with detailed information on each. Unlike the David Horowitz Freedom Center, this list appears to contain only US organizations. There is no attempt to link these groups to foreign or domestic terrorist organizations. The site describes their effort this way:

“Right Wing organizations come in all shapes and sizes, from think tanks to legal groups, local and national lobbying organizations, foundations and media forums. At any given moment, the Right is at work in our public school systems, courthouses, in Congress and state assemblies. At the same time, right-wing groups are reaching huge audiences through media outlets they own or influence — promoting regressive policies that seek to drive wedges between and among Americans.”

So regressive policies and promoting division among citizens is the worst this group has to say about right wing organizations.

Political Research Associates also provides a list of right wing organizations similar to the one at the PFAW. This list is far less detailed. It doesn’t include foreign or terrorist organizations. There are no militia groups, or hate groups or overtly raciest organizations on the list as far as I can tell. It doesn’t include the Aryan Nation or the Klu Klux Klan, for instance.

This isn’t an exhaustive survey, of course. It’s just an exercise. But on the face of things it does appear that some tax exempt organizations have a very political agenda. It also seems that conservative leaning non-profits are more overtly political and include more information of questionable educational value. The problem of political activity among tax exempt groups seems asymmetrical. The added value to the public worthy of extending tax credits to these, or to any overtly political organization is dubious.

Does the IRS have the personnel and resources to properly handle their workload?

According to the IRS, the answer is no. IRS funding was held flat for three years between FY 2005 and 2007. There was a 2.5% cut in its 2012 budget and now it is being squeezed by budget cuts and the sequestration, prompting protests by IRS personnel. There is also this summary of the IRS situation prior to the last two years of budget cuts:

The most serious problem facing U.S. taxpayers is the combination of the IRS’ expanding workload and the limited resources available to the IRS to handle it. Among the consequences:

• the IRS is unable to adequately meet the service needs of the taxpaying public. [it’s only funded at an 80% level for this service.]

• the IRS is unable to adequately detect and address noncompliance, requiring honest taxpayers to shoulder a disproportionately large share of the tax burden.

• the IRS is unable to maximize revenue collection, contributing to the federal budget deficit.

—National Taxpayer Advocate, 2011 Annual Report to Congress

So the answer to this question seems to be no. This gives credence to claims that IRS line staff were triaging tax exempt applications to better handle their workloads. It also suggests that the problem of the huge collection gap, between what is owed and what is paid, won’t be fixed anytime soon. It has been estimated by the IRS’s own computer analysis that there are about a million tax returns each year that appear to contain fraudulent information but are not audited. At a time when the federal government is starving for revenue the anti-tax sentiments in congress seem to extent to collection of legally due taxes, not just tax increases.

Finally, is IRS agents to determine the degree of political activity permitted by current IRS regulations an impossible job?

The answer to this last question is yes, it is absolutely impossible. In the increasingly polarized politics of today there are often disagrements on who is a liberal or a conservative. The two camps can’t even on a common set of facts for any given topic. How can the IRS possibly create a suitable metric for deciding which 501(c)(4) organizations have crossed the political line. Even more importantly, why is the IRS even trying to make room for political activity for tax exempt organizations? The clear intent of the law excludes the from any political activity at all. This is what tax payers should demand in exchange for the tax break these organization receive from us.

Here then is the real scandal. The IRS, one of the most fundamental agencies in government, is under staff and without resources by congressional design at a time when it faces massive fraud and abuse, growing anti-tax sentiments and a groundswell of people and organizations trying to claim tax exemptions for overtly political purposes. It is trying to police this latter situation with an unenforceable and illegal regulation that it has been saddled with for over 60 years. Why isn’t this the real IRS scandal?

Tax Breaks Cost US More Revenue than Medicare, Defense or Social Security

Tax breaks, also know as federal tax spending, includes things like mortgage deductions, child tax credits and lowered tax rates on capital gains. The CBO published a report today on what these deductions and tax breaks cost the federal government in annual revenues. The total amount is enormous. The top 10 most revenue syphoning tax cuts (there are more than 200 tax deductions in all) cost $900 billion. Tax spending is greater than budge expenditures for Medicare, Defense, or Social Security. It equals 1/17th of the US economy (or GDP). But taxbreaks or loopholes don’t show up anywhere in the federal budget, so the relative size of these hidden expenses are not usually apparent. They don’t often make it into the national dialogue when we talk about the budget. Below is the CBO report summary.

congressional budget office

supporting the congress since 1975

http://cbo.gov/publication/43768

The Distribution of Major Tax Expenditures in the Individual Income Tax System

report date: May 29, 2013

A number of exclusions, deductions, preferential rates, and credits in the federal tax system cause revenues to be much lower than they would be otherwise for any given structure of tax rates. Some of those provisions—in both the individual and corporate income tax systems—are termed “tax expenditures” because they resemble federal spending by providing financial assistance to specific activities, entities, or groups of people. Tax expenditures, like traditional forms of federal spending, contribute to the federal budget deficit; influence how people work, save, and invest; and affect the distribution of income.

This report examines how 10 of the largest tax expenditures in the individual income tax system in 2013 are distributed among households with different amounts of income. Those expenditures are grouped into four categories:

- Exclusions from taxable income—

- Employer-sponsored health insurance,

- Net pension contributions and earnings,

- Capital gains on assets transferred at death, and

- A portion of Social Security and Railroad Retirement benefits;

- Itemized deductions—

- Certain taxes paid to state and local governments,

- Mortgage interest payments, and

- Charitable contributions;

- Preferential tax rates on capital gains and dividends; and

- Tax credits—

- The earned income tax credit, and

- The child tax credit.

Some of the provisions of law that reduce the amount of taxable income under the individual income tax also decrease the amount of earnings subject to payroll taxes. The figures presented in this report are generally based on the reduction in payroll taxes as well as the reduction in income taxes, but some figures separate those two effects. (Provisions that reduce payroll tax receipts generally reduce future Social Security benefits as well; that effect is not analyzed in this report.)

How Do Tax Expenditures Affect the Federal Budget?

Although the 10 major tax expenditures listed here represent a small fraction of the more than 200 tax expenditures in the individual and corporate income tax systems, they will account for roughly two-thirds of the total budgetary effects of all tax expenditures in fiscal year 2013, CBO estimates. Together, those 10 tax expenditures are estimated to total more than $900 billion, or 5.7 percent of gross domestic product (GDP), in fiscal year 2013 and are projected to amount to nearly $12 trillion, or 5.4 percent of GDP, over the 2014–2023 period. In addition, tax credits to subsidize premiums for health insurance provided through new exchanges to be established under the Affordable Care Act will represent a new tax expenditure beginning in 2014, estimated to equal 0.4 percent of GDP over the 2014–2023 period.

How Are Tax Expenditures Distributed Among Households?

The 10 major tax expenditures considered here are distributed unevenly across the income scale. In calendar year 2013, more than half of the combined benefits of those tax expenditures will accrue to households with income in the highest quintile (or one-fifth) of the population (with 17 percent going to households in the top 1 percent of the population), CBO estimates. In contrast, 13 percent of those tax expenditures will accrue to households in the middle quintile, and only 8 percent will accrue to households in the lowest quintile (see the top panel of the figure below).

When measured relative to after-tax income, those 10 major tax expenditures are largest for the lowest and highest income quintiles. In calendar year 2013, CBO estimates, the combined benefits will equal nearly 12 percent of after-tax income for households in the lowest income quintile, more than 9 percent for households in the highest quintile, and less than 8 percent for households in the middle three quintiles (see the bottom panel of the figure above).

The distribution of tax expenditures across the income scale varies considerably among the different tax expenditures. For example, CBO estimates that more than 90 percent of the benefits of reduced tax rates on capital gains and dividends will accrue to households in the highest income quintile in 2013, with almost 70 percent going to households in the top percentile. Those benefits will equal 2 percent of after-tax income for the highest quintile and 5 percent of after-tax income for households in the top percentile. In contrast, about half of the benefits of the earned income tax credit will accrue to households in the lowest income quintile, equaling 6 percent of after-tax income for households in that group.

Tax credits that will provide assistance in paying premiums in health insurance exchanges are excluded from the distributional results presented here because they are not in effect in 2013. When those tax credits come into effect, they will appreciably increase tax expenditures for households in the lower and middle income quintiles. Individuals and families who have income between 100 percent and 400 percent of the federal poverty guidelines and who meet certain other requirements will be eligible for those credits.

How Do Tax Expenditure Estimates Differ From Revenue Estimates?

Estimates of tax expenditures are traditionally intended to measure the difference between households’ tax liabilities under present law and the tax liabilities they would have incurred if the provisions generating those tax expenditures were repealed but households’ behavior was unchanged. Such estimates do not represent the amount of revenues that would be raised if those provisions were eliminated, because the changes in incentives that would result from eliminating those provisions would lead households to modify their behavior in ways that would mute the impact on revenues. For example, if the preferential tax rates on capital gains realizations were eliminated, taxpayers would reduce the amount of capital gains they realized. Because the size of that tax expenditure is estimated on the basis of the gains that are projected to be realized with the preferential rates in place, the amount of additional revenues that would be received if those preferences were eliminated would be smaller than the reported tax expenditure.

America’s Social Contract And The Measure of Our Commitment

(Note: contains some material from prior posts)

by Brian T. Lynch, MSW

A key element in America’s social contract is the idea that government derives its authority from the consent of the people. So the question should occasional be asked, is our mutual consent to be governed wearing thin? There is evidence to suggest a growing restiveness in certain populations. Some symptoms of declining consent include gridlock in congress marked by an inability to pass any legislation on a simple majority vote, the resurgence in states’ rights activism, calls in some states for secession, citizens arming themselves in fear (or perhaps the hope) of armed resistance and wide spread efforts to manipulate elections. Perhaps the best, most quantitative way to judge the degree to which we consent (or commitment) to self-government is by our willingness to pay taxes.

The attitudes we have towards paying taxes, and the extent to which people and organizations will go to avoid them, is an underappreciated index of our consent to be governed. Just as taxation without representation was a rallying cry leading up to the Revolutionary War, the Tea Party and many other popular reform or resistance groups today rally around taxes as a central point of contention. Objectively speaking, the Tea Party’s opposition to taxes makes no sense since their complaint corresponded with the lowest federal tax rate since the Eisenhower administration. It isn’t until we understand that our attitude towards taxes is a barometer of our consent to be governed that the Tea Party’s tax objections become clear.

For the sake of discussion it is helpful to identify different segments of the population that are particularly opposed to taxes. But keep in mind that our personal attitude towards paying taxes is just as valid an indicator of where each of us falls on this measure of consent.

Let’s begin with those who see themselves through the lens of American individualism. They value self-reliance and see this as a patriotic duty. They tend to think less of those who are more collaborative, more dependent or less successful. They tend to discount the contribution of the public commons to their own welfare and don’t often recognize how massively interdependent advanced societies really are. They believe that less government is best for everyone. These folks are less willing to contribute to tax supported government services other than for military defense. They are ideological individualist. This group may include some libertarians and on the extreme fringes may also include some anarchists or survivalists.

There are those who are suspicious or uncomfortable with American pluralism. These folks tend to live in parts of the country where there is little diversity or just a single predominate minority group. However, folks who hold this belief can be found everywhere. They believe a disproportionate amount of their taxes go to support other ethnic or cultural groups whose members don’t share their same values or work ethic. They may fear that these other groups are taking advantage of government largess. As a result, they are more resentful of paying taxes and more critical of what they see as wasteful government spending. These folks are pluralism-adverse and at the extreme fringes this group may include racists or hate groups. A highly nationalistic subset of this pluralism-adverse group believe their government has already broken faith with them and is threatening their liberty. For them, paying taxes is akin to paying tribute to a foreign potentate. The most extreme of these consider themselves to be soverign citizens.

There are some religious fundamentalists who believe all secular government is evil. Some fundamentalist sects focus on The Book of Revelations and an apocalyptic view of the world in which governments plays a role in the rise of the false prophet. For these groups anything that expands government is evil as well, including increased taxes. They are usually considered to be on the fringe of the Christian community, but they have an impact beyond their numbers.

Then there are those who believe taxes compete or interfere with commerce and free markets. They believe that taxes reduce the capital available for businesses investments. They fear that more taxes will lead to more government regulations and further hinder commerce. They don’t see government spending as simulative for the economy. For them, the provision of government services to those who aren’t successful contributors is an unfair redistribution of wealth. Members of this group are more likely to have higher incomes and a sense of entitlement. They may pride themselves in their ability to avoid paying taxes. At the extreme fringes of this group members tend to see society as being made up of the have and the have nots, the makers and the takers. They are often contemptuous of taxes and government.

Next, there are the disaffected and those too self-absorbed to care much about government. For this group all taxes are an annoyance to be avoided. This is a large and diverse group that is often underrepresented in our national conversations. They include many who are poor, but also many who are middle class folks working hard just to make ends meet. They tend to be swing voters when they vote and their grasp of politics and government policies are more maliable. The underground cash economy is significant for them.

The impact of this growing reluctance by some citizens to pay income taxes is huge. According to a GAO report called “HIGH-RISK SERIES, An Update”, the Internal Revenue Service estimated that the gross tax gap–the difference between taxes owed and taxes paid on time–was $450 billion for tax year 2006. The IRS estimated that it would collect $65 billion from these taxpayers through enforcement actions and late payments, leaving a net tax gap of $385 billion. This doesn’t include the loss of tax revenue due to the underground cash economy and foreign US cash transactions. These create an additional tax gap estimated to be between $400 billion and $540 billion annually. There is also the tax gap created when wealthy investors hide their money in off shore tax havens. According to a study by the Tax Justice Network the world’s super rich have at least $21 trillion secretly hidden away in tax shelters as of 2010. This is equivalent to the size of the Japanese and United States economies combined, according to The Price of Offshore Revisited report. Further, the amount of secretly hidden wealth may be as high as $32 trillion.

Arguably the most tax resistant groups, which also have the greatest fiscal and political impact, are businesses and corporations. The largest loss of tax revenue, representing the lowest level of consent to be governed, comes from the corporate sector. The shift in the percentage of total federal income taxes paid by individuals verses businesses has grown substantially over the years. Individual income taxes raised 41% of the total tax revenue in 1943 while business income taxes made up the rest, or more than half of the income tax receipts. Compare this with today where 79% of total revenues comes from individual income taxes. This shift in tax receipts from corporations to individuals cannot be explained by a shift away from C corporations (who pay the corporate income tax) to S corporations (who don’t). According to the financial site NerdWallet, the 10 most profitable U.S. companies paid an average federal tax rate of just 9 percent in 2011. The group includes such giants as Exxon Mobil, Apple, Microsoft, JPMorgan Chase and General Electric. The Economist recently posted a graphic by the Bureau of Economic Analysis that depicts the decline in corporate taxes juxtaposed to the rise in corporate profits.

The inability of the federal government to collect taxes from the nation’s elite and its biggest corporations is a serious sign of trouble. It signals a real strain in our social contract and severly limits the ability of the government to serve its people. The problem is compounded by the fact that anti-tax sentiments are being exploited by wealthy business interests to ferment dissatisfaction and distrust of our government. A coalition of the most anti-tax, anti government constituents from the various tax adverse segments of society described above would look very similar to the Tea Party base of today’s Republican Party. The power we invest in civil government is the only check we have to balance the power of the largest corporations to do as they wish in pursuit of profits. It would be a mistake to weaken our commitment to good government now when it is under assault.

There are still many who believe taxes are the price we must pay for a just and robust society. Paying taxes is our civic duty and evidence of our commitment to one another. It reflects confidence that our government is representing us and upholding the social contract. The present IRS scandal over the targeting of Tea Party groups for selective scrutiny of their 503(c)4 tax status is really a minor but convenient distraction from the real tax crisis we face. We are facing a crisis of confidence in self-government. It is a challenge of our time to rekindle a popular passion for civil government that is truly of, by and for the people.

Taxes and America’s Social Contract

The American social contract is threadbare in certain parts of America. Areas of this great country are falling into disrepair, dissolution as if under a spell . In places like the Camden, New Jersey and now Josephine County, Oregon, public safety has been compromised by the failure of will to raise taxes. Below you will find a very disturbing report on the latter situation from Oregon Public Broadcasting. It dramatically highlights what can go wrong when citizens can’t make the connection between good government and the tax revenue it takes to have it. First, let’s consider the various segments of our population who oppose raising taxes.

There are those who see themselves through the lens of American individualism. They value self-reliance and see this as a patriotic duty. They tend to think less of those who are more collaborative or more dependent or unsuccessful. They tend to discount the contribution of the public commons to their own welfare and don’t often recognize how massively interdependent our advanced society really is. They believe that less government is best for everyone. These folks are less willing to contribute to tax supported government services other than for military defense. They are ideological individualist. They may include libertarians. On the extreme fringe they may include anarchists or survialists.

There are those who are suspicious or uncomfortable with Ameican pluarism. These folks most often live in parts of the country where there is little diversity or only a single other minority group. But folks who hold this belief can also be found everywhere. They believe a disproportionate amount of their taxes go to support other ethnic or cultual groups whose members don’t share their same values or work ethic. They sometimes fear other groups are taking advantage of government largess. As a result, they are more resentful of paying taxes and more critical of wasteful governement spending. They are pluralism-adverse. At the extremes this group may include racists and hate group. A highly nationalistic subset of this pluralism adverse group believes the federal government has already broken faith with the people and threat our liberty. For them, paying taxes is akin to paying tribute to a foreign potentate.

There are some religious fundamentalists who believe all secular government is evil. For them, anything that expands government is evil as well, including raising taxes.

There are those who believe taxes compete or interfere with commerce and the free market. They think that taxes only reduce the capital available for business and contribute to government regulations. They don’t see government spending as stimulating for the economy. For them, the provision of services to those who aren’t successful contributors to the economy is an unfair redistribution of wealth. This group are more likely to have higher incomes and to pride themselves in their ability to avoid paying taxes. In the extreme they tend to see society as made of the have and have nots, the makers and the takers.

I believe all these groups are being aggitated and moulded into an anti-government political movement to reduce the power of government to regulate powerful corporate interests. But regardless of what you or I believe, the truth of who we are becoming is reflected in the hopes and fears of this 911 caller in Josephine County, Oregon.

With No Officers To Respond To 911 Calls, Josephine Co. Considers Tax Levy

OPB | May 14, 2013 3:40 p.m. | Updated: May 15, 2013 10:50 a.m. | Grants Pass, Oregon

http://www.opb.org/news/article/josephine-county-tax-levy-would-add-deputies-fund-the-jail/

Corporate Taxes Fall as Profits Soar

The Economist states it just right. Big corporations are avoiding their tax obligation. They have no sense of duty or obligation towards the peoples government which created corporations and the condition in which they have flourished. Increasingly, government is a gadfly to corporate profit making as citizens insist, through their government, that we breath clean air, drink pure water and eat healthy foods. Corporations are so large and powerful today that the only checks on their power is big government… hence the sustained attacks they are waging on big government. But when governments no longer have the power or ability to collect taxes from the elite or the largest corporations, they are close to colapsing. That is the message I take away from this latest report. I encourage everyone to go there and read more.

Taxing for some

America’s corporation-tax receipts falter even as company profits soar

THE pressure on tax-avoiders is mounting. In the latest episode Tim Cook, Apple’s boss, was called before a Senate subcommittee to explain why the tech giant had paid no tax on $74 billion of its profits over the past four years—though it has done nothing illegal. This comes at a time when America’s corporate profits are at a record high, thanks to the swift sacking of workers at the start of the recession, lower interest expenses, and the fact that cheap labour in emerging markets has eroded union power, allowing firms to move production offshore and defy demands for pay rises. Meanwhile corporation tax, which makes up 10% of the taxman’s total haul (down from about a third in the 1950s) has plummeted. An increase in businesses structuring themselves as partnerships and “S” corporations, which subject profits to individual rather than corporate income tax, is in part to blame. But tax havens are also culprits, as they lower their tax levels to lure in bigger firms.

Does Philanthropy End Up Hurting the Poor and Vulnerable?

What follows is my response to an open discussion about the role and social value of philanthropic foundations. It is my response to the lead article by Dr. Rob Reich, which can be read in its entirity at the URL below.

BOSTON REVIEW

http://www.bostonreview.net/BR38.2/ndf_rob_reich_foundations_philanthropy_democracy.php#c5t_form

Lead Essay:

What Are Foundations For?

Rob Reich

This article leads off our debate on philanthropy, with responses from Stanley Katz, Diane Ravitch, Larry Kramer, and others.

Graham Smith

Graham Smith

Judge Richard Posner, one of the foremost American jurists outside the Supreme Court, once observed, “A perpetual charitable foundation . . . is a completely irresponsible institution, answerable to nobody. It competes neither in capital markets nor in product markets . . . and, unlike a hereditary monarch whom such a foundation otherwise resembles, it is subject to no political controls either.” Why, he wondered, don’t we think of these foundations as “total scandals”?

If foundations are total scandals, then we have a massive problem on our hands. We are now living through the second golden age of American philanthropy. What Andrew Carnegie and John D. Rockefeller were to the early twentieth century, Bill Gates and Warren Buffett are to the early twenty-first century.

The last decade of the twentieth century witnessed the creation of unprecedentedly large foundations, such as Gates’s. The assets of the Gates Foundation and a separate Gates Trust, which holds wealth donated by the Gates family and Buffett, together total more than $65 Billion. If the combined entities were a nation, it would be 65th on the world GDP list. And it’s not just billionaires and their mega-foundations that command attention. Record wealth inequalities might be a foe to civic comity, but they are good for philanthropy. The boom in millionaires has fueled unprecedented growth in the number and assets of small foundations as well.

So foundations have seen explosive growth. But why are they a scandal? Read the Full Article. http://www.bostonreview.net/BR38.2/ndf_rob_reich_foundations_philanthropy_democracy.php#c5t_form

My Comments:

In setting up his essay on philanthropic foundation in this “second golden age”, Reich offered the following: “Let us dismiss quickly one common and intuitive thought: that foundations exist because they are remedial or redistributive, responsive to the needs of the poor or disadvantaged.”

He goes on to identify public goods this way: “It has long been understood that the commercial marketplace does not do well at providing what economists call public goods. These are goods that, like a well-lit harbor, are available to everyone if they are available to anyone; and that, like clean air, do not cost more when they are consumed by more people. “

After three decades in the field of child welfare, this was a startling and insightful dismissal. In debating whether America’s philanthropic foundations are worthy of the tax exempt status conferred on them in 1937, Reich excludes consideration of their value relative to public services that reduce human misery but carry a cost per use. In other words Reich’s definition of public goods includes only passive public services, like street lights, but not active public services, including child welfare. This certainly explains why foundational giving for public needs is so small a percentage of their activity. Yet we are asked to judge whether their social contribution is worth their $53 billion in tax exemptions each year? How much good could that revenue do to support and strengthen our most vulnerable citizens? Don’t ask!

To characterize social services as remedial “or redistributive” of wealth, is offensive to me. When used to characterize government spending on the general welfare, “redistribution” is a code word to frame partisan arguments in our muffled debate over distributive justice. Taxing the more successful citizens to promote the general welfare, except for military spending, is considered an unfair redistribution of wealth, yet any discussion on the fair distribution of profits between workers and business owners is considered out of bounds.

The context for this discussion on foundations is the social value of philanthropy at a time when wealth disparity has never been greater. When a growing number of wealthy foundations are extracting ever more revenue from an already dwindling federal revenue stream, excluding consideration of their impact on public services makes this discussion itself a plutocratic exercise.

The pros and cons of whether foundations generate valuable diversity and innovation were well explored by the forum’s other contributors, but none of their essays addressed underlying assumptions. Foundations actually do play an outsized and often deterious role in how community social services are structured, funded and distributed. None of the contributors picked the scab off this wound to consider the broader picture. Financially speaking, foundations are in direct competition with public social services and the vulnerable populations served. I was disappointed.

CLASS WARFARE – OVERVIEW OF WAGES, TAXES and WEALTH IN AMERICA

Since Reagan in 1980’s Tax Rates for the wealth were cut in half and capital gains tax (where most make their money) was cut in half again. http://j.mp/ZFFQHB

Wages and GDP rose together until wages were suppressed in the 70’s, otherwise median income today would be greater than $100K instead of $51K http://j.mp/14MoT67

The combination of wage suppression and the collapse of the upper income tax brackets is the cause of our wealth and income inequality today. http://j.mp/102YbAk and http://j.mp/10DVrLn

A majority of American’s don’t make enough money to support a robust economy because a handful of us have more money than they can spend. http://j.mp/16E3zOT

Current US policy is creating permanent income inequality. Income mobility is shrinking as income caste system forms. http://t.co/nK5uFGyCaG

We know what victory looks like in Class Warfare. It’s the formation of an income caste system where birth determines your level of success. http://j.mp/Y1HwQP

Obama’s proposed raise in min. wage from $7.20 to $9/hr would mean a person working 40hr/week at min. wage would still be below poverty line. http://j.mp/10DwY7V

If the minimum wage was raised to $18/hour the Federal Government could eliminate almost all aid to the working poor, saving tons of money. http://j.mp/10DVrLn

Every tax dollar paid to assist the working poor is a tax subsidy providing their employer a federally funded labor discount. http://j.mp/16Bml7r

God! When are we going to wake up?