by Brian T. Lynch, MSW

College graduates have always earned more in their lifetime than non-college graduates, but higher tuition costs is increasing borrowing and the higher interest rates on these loans is taking a bit out of their future. In addition, there continues to exist a higher unemployment rate for college graduates.

The Federal Reserve Bank of New York just released its quarterly Household Debt report. It reveals that non-housing debt is rising and student loans are a big contributor. Non-housing debt increased 2.8% since last quarter and 4.9% from a year ago. Housing debt decreased 1.9% from a year ago.

Looking at just the non-housing debt, student loans account for 36% of the total, up a percent from a year ago. Auto loan debt is increasing faster over the last year and now accounts for 30% of all non-housing debt. Student loan debt rose 4% from the last quarter and 7.29% from a year ago. Meanwhile credit card debt is unchanged over the past 12 months while other forms of non-housing debt declined by over 3%.

The Federal Reserve also reported good news that 90-day delinquency rates on household debt has declined. For the banking industry it is a twin blessing when borrowing rises and delinquency falls. For consumers it is a mixed blessing, at best. But, when you look at the particular, it is immediately clear that college educated adults are in serious trouble. They are defaulting as never before. Look at the line graph below and you will see what I mean. The student loan default is the red line that starts as the third highest default rate in 2004 to exceed credit card and auto loan defaults as of last year.

Source: Fed Report http://www.newyorkfed.org/regional/householdcredit.html

According to the Fed report, outstanding student loan balances increased to $1.027 trillion as of September 30, 2013, a $33 billion increase from the second quarter. The 90+ day delinquency rate increased, and is now at 11.8%.

Full Report: http://www.newyorkfed.org/research/national_economy/householdcredit/DistrictReport_Q32013.pdf

Higher tuition costs means greater borrowing which results in higher monthly payments on the debt. The high rate of unemployed, or underemployed college graduates is part of the reason for the higher default rates. What follows is a snippet from an excellent article in the Atlantic Monthly. (Go there to read it in full)

How Bad Is the Job Market For College Grads? Your Definitive Guide

JORDAN WEISSMANN APR 4 2013

They’re Better Off Than High School Grads … Bachelor’s holders (in blue below) have about half the unemployment rate of high school graduates (in red below). BA’s are still suffering from double the low rate of joblessness they enjoyed pre-recession. And yes, they’re even worse off than they were during the tepid economies of the early nineties or pre-housing bubble oughts. But on the whole, you’d much rather have a degree in this job market than not.

But They’re Still Hurting… That’s all bachelor’s holders, though (or at least the ones over 25, who the Bureau of Labor Statistics routinely tracks). So what about young adults just off campus? The numbers aren’t a nightmare, but they aren’t especially pleasant either. Last month, the Bureau released a special report looking at Americans under 30 who’d earned a bachelor’s in the past year, as of October of 2011. About 73 percent were employed (the paper didn’t specify between full time and part-time). More than 11 percent were still looking for work.

In addition to the higher rate of unemployment, rising tuition costs over the past decade has meant larger monthly payments. College tuition costs have even risen faster than medical costs, and much faster than the consumer price index. Below is a very clear graphic depiction of this from Professor Mark J. Perry out of the University of Michigan.

Professor Mark J. Perry’s Blog for Economics and Finance

The chart above illustrates graphically the “higher education bubble” by comparing the annual increases in the CPI for “College tuition and fees” (7.45% per year since 1978) to annual increases in the CPI for “medical care” (5.8% per year since 1978) to annual increases in the median price for new homes (4.3% per year) to the annual increases in the “CPI for all items” (3.8% per year)

[See more at: http://mjperry.blogspot.com/2011/07/higher-education-bubble-college-tuition.html#sthash.HF1DSyOu.dpuf ]

The good news, according to the Trends in Education Website, is that the rate of tuition increases is declining. Here below is a snippet from their Website.

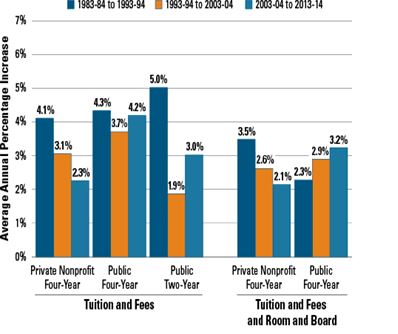

Average Rates of Growth of Published Charges by Decade

The 2.9% one-year increase in average published tuition and fees for in-state students at public four-year institutions in 2013-14 was 0.9% after adjusting for inflation. This relatively small increase in prices means that despite very large annual increases earlier in the decade, tuition inflation between 2003-04 and 2013-14 was similar to that between 1983-84 and 1993-94.

Figure 4: Average Annual Percentage Increases in Inflation-Adjusted Published Prices by Decade, 1983-84 to 2013-14

See Key Points|See Also Important

Each bar in Figure 4 shows the average annual rate of growth of published prices in inflation-adjusted dollars over a 10-year period. For example, from 2003-04 to 2013-14, average published tuition and fees at private nonprofit four-year colleges rose by an average of 2.3% per year beyond increases in the Consumer Price Index.

A third reason why so many college students are unable to pay their loans is the rising cost of financing those loans. Karen Weise recently wrote a an article in Business Week that laid out the problem of higher student loan rates. A snippet appears below.

Why Your Student Loan Interest Rate Is So High

By Karen Weise April 04, 2013

Business Week

Joe Szczepaniak pays a 3.5 percent interest rate on the mortgage for his house in a Chicago suburb. His car loan is 1.79 percent. The federal education loans he took out to send his four sons to college? They’re all above 7 percent. “Student loans have been the big black holes of my budget,” he says. Szczepaniak, who calls himself “Mr. Quicken” because he carefully tracks his finances, questions why the $200,000-plus he owes on the student loans doesn’t “reflect reality” and today’s low rates.

The answer is that Congress, not the market, sets rates for federal loans—which account for 85 percent of the roughly $1 trillion in outstanding education debt—and refinancing to a lower rate is rarely an option. Now some lawmakers and private lenders are looking for ways to give education borrowers more repayment and refinancing options.

[Read more at http://www.businessweek.com/articles/2013-04-04/why-your-student-loan-interest-rate-is-so-high ]

Student loan rate had been set to double, so congress acted to mitigate the sudden increase that was to occur. There is good information on the Consumer Financial Protection Bureau Website detailing the recent changes. An update on government student loan interest rates was recently published (see below). At a time when I can get a car loan from my credit union with an interest rate below 3%, our college students can’t get a federally subsidized student loan for under 3.86%, and private bank loans for students is even higher.

Consumer Financial Protection Bureau

Updated on August 13, 2013:

Last week, the president signed legislation passed by Congress to adjust federal student loan interest rates for this academic year. Here’s what the new rates look like:

http://www.consumerfinance.gov/blog/changes-to-federal-student-loan-interest-rates/

We have to stop and ask ourselves what the long term impact will be on our children and our economy if we don’t do more to make college affordable.